Introduction

PE sponsors routinely stress-test financial models, interrogate commercial assumptions, and negotiate reps and warranties with precision. Vendor risk tends to get a fraction of that attention — and the gap shows up after close.

Third-party vendors across IT, logistics, procurement, and professional services can quietly erode EBITDA through poor contract controls, trigger regulatory exposure through their own non-compliance, or create operational disruptions that stall value creation timelines. These aren't edge cases — they're post-close realities that compress margins and extend hold periods.

Addressing that gap requires a structured approach — not a one-time diligence checkbox. This guide gives PE sponsors, operating partners, and portfolio company leadership a practical framework covering what vendor risk assessment is, why it directly affects returns, how to execute it, and how to scale this capability across a portfolio. It also covers how firms like Colab91 help mid-market portfolio companies run this continuously without building a large onshore team.

Key Takeaways

- Vendor risk spans financial, operational, compliance, cybersecurity, and ESG exposure — not just IT security

- Risk accumulation happens primarily during the hold period, not at close

- Sophisticated buyers routinely use unmanaged vendor dependencies to justify valuation adjustments or escrow provisions

- Mid-market portfolio companies can run effective vendor risk programs with offshore, domain-expert-led teams — without relying on stretched generalist staff

What Is a Vendor Risk Assessment in the Private Equity Context?

A vendor risk assessment is the structured process of identifying, scoring, and managing the risks that third-party vendors introduce into a business. It spans financial, operational, cybersecurity, compliance, and reputational dimensions — and it applies across the full vendor lifecycle, not just at contract signing.

In a PE context, this definition carries an additional layer. A portfolio company's vendor risk becomes the fund's risk. Vendor failures compress EBITDA and erode valuation; compliance gaps threaten exit readiness; unaddressed concentration risk undermines LP confidence.

The PE sponsor therefore has both financial and governance incentives to ensure portfolio companies maintain defensible vendor oversight.

This goes beyond a standard procurement review. Vendor risk assessment is not about price or contract terms alone — it addresses systemic exposure across four categories:

- Single-source dependencies with no viable fallback

- Data access granted to third parties

- Regulatory co-liability across jurisdictions

- Operational concentration risks embedded in the supply base

Colab91's Supplier Risk Management platform is built around continuous monitoring rather than periodic reviews. It tracks supplier financial health, sanctions and OFAC exposure, ESG compliance, regulatory risk, and cyber/data risk — with risk scores tied directly to spend so each exposure carries a dollar figure, not just a color-coded flag.

Why Vendor Risk Is a PE Value Issue, Not Just a Compliance Checkbox

The Post-Close Leakage Problem

Vendor relationships are a leading source of post-close value leakage. Unmonitored third parties drive cost overruns through weak contract controls, create supply disruptions when a key vendor's financial position deteriorates, and trigger regulatory penalties when their non-compliance becomes the portfolio company's liability. Each of these events compresses EBITDA and extends hold periods.

Add-on acquisitions amplify this. According to CBH's Private Equity Report, add-ons represented nearly 80% of total PE deal count by 2022. As each acquisition integrates, vendor bases multiply. Firms that don't reassess vendor risk post-integration frequently discover overlapping critical vendors, compliance gaps, and data security vulnerabilities that were invisible at the individual company level.

LP and Regulatory Expectations

LPs now ask explicit questions about vendor oversight. The ILPA DDQ 2.0 requires managers to disclose:

- Third-party service providers used over the prior five years

- Whether those vendors are subject to security reviews and independent assessments

- Control reports — such as SSAE 18 or ISAE 3402 — from key third parties

These aren't optional disclosures. They're standard LP due diligence, and gaps in vendor documentation will surface during fundraising.

Regulators have moved in the same direction. The SEC's FY2025 exam priorities explicitly flag oversight of third-party products, subcontractors, and services as an examination area. The 2024 Regulation S-P amendments require registered investment advisers to maintain written policies for service-provider oversight — covering documented due diligence and ongoing monitoring. Vendor oversight is now a regulatory expectation, not a best practice.

Exit Risk

Strategic and financial buyers in secondary transactions now conduct thorough third-party risk reviews. When they find undocumented vendor dependencies, unresolved compliance gaps, or single-vendor concentration, those findings go into management presentations — and buyers use them to justify valuation adjustments, escrow provisions, or deal protections.

A well-documented vendor risk program doesn't just protect operations — it directly supports a cleaner, faster exit.

Key Vendor Risk Categories PE Firms Must Evaluate

Financial Risk

A vendor's financial instability can create sudden supply disruptions that derail operations. Allianz Trade's 2025 Insolvency Report shows global business insolvencies rose 10% in 2024 and are forecast to rise a further 6% in 2025. For single-source or mission-critical vendors, a sudden failure has no easy recovery path. Financial health monitoring is a baseline requirement for any high-tier vendor relationship, not an occasional check.

Operational and Concentration Risk

Over-reliance on a single vendor for a critical function represents a quantifiable operational risk. This category frequently surfaces during post-close integration when two merged companies share the same critical IT vendor — a concentration that only becomes visible once it has already caused disruption. Three factors require active assessment, not assumption:

- Geographic concentration of supplier base

- Single-source dependencies for critical functions

- Absence of qualified alternative suppliers within acceptable lead times

Compliance and Regulatory Risk

Vendors operating in regulated environments can expose portfolio companies to shared liability. The enforcement record makes the stakes concrete:

- HIPAA business associate liability: HHS OCR's Catholic Health Care Services settlement imposed a $650,000 penalty on a business associate providing IT and management services to nursing homes following a data breach

- FCPA third-party exposure: The DOJ's SAP resolution required payment of over $220 million in connection with FCPA violations involving third-party intermediaries

GDPR/CCPA processor obligations create a parallel exposure for any vendor handling customer data. Regulatory liability follows the data, not the org chart.

Cybersecurity and Data Risk

According to the IBM Cost of a Data Breach Report 2025, supply chain compromise accounted for 15% of attack vectors with an average breach cost of $4.91 million. The Verizon DBIR 2024 reported the same 15% figure for breaches involving a supply-chain interconnection.

For PE firms specifically, vendors with access to LP data, deal information, or portfolio financials represent a concentrated cybersecurity exposure. The SEC has identified third-party vendor cybersecurity as a priority examination area in both its FY2024 and FY2025 priorities.

Reputational and ESG Risk

PwC's 2023 Global Private Equity Responsible Investment Survey found that 70% of PE firms rank value creation as a top-three driver of ESG activity, and 91% report active responsible investment programs. KPMG's 2024 ESG Due Diligence study found 82% of global dealmakers have ESG on their M&A agenda.

Vendors with labor violations, environmental non-compliance, or governance failures generate reputational damage that affects brand value, customer retention, and future fundraising. For PE firms, supply chain ESG risk belongs in diligence and hold-period reviews — by exit, the damage is already priced in.

How to Conduct a Vendor Risk Assessment: Step-by-Step

Step 1: Build a Complete Vendor Inventory

Most mid-market portfolio companies lack a clean, centralized vendor list. The first task is compiling a complete inventory of active vendors, segmented by:

- Spend (annual and lifetime contract value)

- Business criticality (what breaks if this vendor fails?)

- Data access level (what systems, customer data, or financial records can they reach?)

- Function (IT, logistics, professional services, raw materials)

This inventory is almost always more complex than expected. It typically surfaces previously unknown single-source dependencies and reveals vendor relationships that exist outside any formal procurement process.

Colab91's spend analytics platform supports this step by cleansing and classifying spend data to UNSPSC or client-specific taxonomy standards, then layering in supplier risk profiles and contract terms — giving teams a structured starting point rather than a raw data dump.

Step 2: Tier and Prioritize Vendors by Risk Exposure

Not every vendor warrants the same scrutiny. A risk-tiering model combines spend and criticality with inherent risk factors:

| Tier | Profile | Assessment Depth |

|---|---|---|

| Critical | High spend, single-source, sensitive data access, regulated sector | Deep-dive review, annual minimum |

| Elevated | Moderate spend, some substitutability, compliance exposure | Structured assessment, 18-month cycle |

| Standard | Low spend, easily replaceable, no data access | Lighter-touch periodic review |

Tiering is what makes a vendor risk program manageable. Without it, teams either over-invest in low-risk vendors or under-invest across the board.

Step 3: Collect and Verify Vendor Data

Risk questionnaires provide a starting baseline. They should not be the only source. Self-reported data must be supplemented with:

- Audited financial statements and credit scores (Dun & Bradstreet and equivalent)

- Third-party certification records (SOC 2, ISO 27001, HIPAA attestations)

- Regulatory filings and sanction screening results

- Independent reference checks

Self-assessment alone is insufficient because vendors have an obvious incentive to present favorably. Colab91's platform integrates D&B data, OFAC/sanctions screening, and ESG compliance signals as third-party verified data sources, reducing dependence on vendor-reported information.

Step 4: Score and Rank Risk

Use a Likelihood × Impact model to assign risk scores. This approach distinguishes between:

- Inherent risk: The vendor's baseline exposure based on profile, geography, industry, and data access — before any controls are applied

- Residual risk: Remaining exposure after existing controls, certifications, and contractual protections are factored in

Ranking the vendor population produces a prioritized action list. Leadership can act on it. Risk scoring connected to spend — rather than assessed independently — is particularly valuable in PE contexts because it quantifies the financial exposure associated with each risk, not just its severity.

Step 5: Drive Corrective Action and Monitor Continuously

Assessment outputs must connect to action. High-risk vendors require:

- Formal corrective action plans with defined timelines

- Named accountability at both the vendor and portfolio company level

- Measurable milestones that can be tracked between formal cycles

Between annual reviews, continuous monitoring keeps risk profiles current. This means news alerts, financial distress signals (credit score changes, late payment patterns), regulatory change notifications, and ESG incident tracking. Risk profiles go stale quickly. A vendor that passed last year's assessment may be in financial distress or under regulatory investigation today.

For mid-market portfolio companies without dedicated procurement or risk staff, running this at the required depth and frequency isn't feasible with internal generalists.

Colab91 addresses this gap: the firm's India-based offshore teams combine domain expertise in strategic sourcing and spend analytics with an AI-powered Supplier Risk Management platform that delivers continuous monitoring with automated alerting on score changes. PE operating partners get portfolio-wide visibility without building a large onshore risk function at each company.

Building a Portfolio-Level Vendor Risk Program

Why the Fund-Level View Matters

Individual company vendor risk assessments miss a critical dimension: concentration at the fund level. When multiple portfolio companies share the same IT managed service provider, cloud platform, or logistics partner, a single vendor failure creates simultaneous disruption across the portfolio. That's not a company-level risk — it's a fund-level exposure.

Beyond risk, a cross-portfolio view creates collective buying power. Common vendors across multiple holdings open the door to:

- Consolidated spend and volume-based renegotiation

- Preferred vendor programs unavailable to individual companies

- Standardized contract terms that reduce legal exposure portfolio-wide

Standardize Without Over-Centralizing

The most effective portfolio-level programs establish:

- A shared risk taxonomy that every company uses to classify vendors consistently

- A common scoring methodology that enables cross-portfolio comparison

- Flexible application that allows each company to adapt the framework to its specific vendor base and regulatory environment

This balance matters most in mid-market portfolios, where individual companies rarely have large procurement teams. The framework has to be rigorous enough for fund-level aggregation — and lean enough to execute without dedicated headcount at every holding.

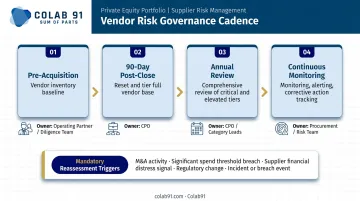

Governance and Cadence

A vendor risk program without clear ownership degrades quickly. Recommended cadence and governance:

| Stage | Activity | Owner |

|---|---|---|

| Pre-acquisition | Vendor inventory baseline | Operating partner / diligence team |

| 90-day post-close | Reset and tier full vendor base | Portfolio company CPO / Colab91 |

| Annual | Comprehensive review of critical and elevated tiers | Portfolio company lead |

| Continuous | Monitoring, alerting, corrective action tracking | Offshore capability team |

Mandatory reassessment triggers — add-on acquisitions, significant contract changes, vendor security incidents, regulatory changes in the vendor's sector — should override scheduled cycles. Waiting for the annual review after a vendor breach or a major add-on close is how exposure compounds into crisis.

Frequently Asked Questions

How do you perform a supplier risk assessment?

Build a complete vendor inventory, tier vendors by spend and inherent risk exposure, collect and verify vendor data from both self-reported and independent sources, score risk using a Likelihood × Impact model, and drive corrective action with continuous monitoring between formal cycles. These steps scale whether you're assessing ten vendors or ten thousand.

What are the key steps in the risk management process?

Identification, assessment and scoring, prioritization, mitigation and corrective action, and ongoing monitoring. In PE, this process must run continuously through the deal lifecycle, not as a one-time pre-close exercise. The hold period is where risk accumulates — and where the process matters most.

What makes vendor risk assessment different for private equity?

PE-backed companies must assess vendor risk through a value creation lens, because vendor failures affect EBITDA, exit valuation, and LP confidence. The PE fund also carries portfolio-level exposure that requires aggregation across holdings. A standalone enterprise manages only its own vendor base; a PE fund must manage risk across all of them simultaneously.

How often should PE-backed portfolio companies conduct vendor risk assessments?

Critical and elevated-tier vendors warrant at least annual formal assessments, with continuous monitoring between cycles. Standard vendors can run on lighter, less frequent schedules. Mandatory reassessment triggers include add-on acquisitions, significant vendor contract changes, and any reported security or compliance incident at a key vendor.

How does unmanaged vendor risk affect exit valuation?

Sophisticated buyers look for documented grounds to justify valuation adjustments, escrow requirements, or deal protections. Undocumented dependencies, compliance gaps, and weak oversight documentation hand them exactly that leverage. A well-documented vendor risk program — covering clear ownership, scoring history, and corrective action records, directly supports a cleaner, faster exit process.