Introduction

PE firms operate under a clock that most businesses don't face. With median hold periods running 5.8 years according to PitchBook, every dollar of controllable spend directly shapes EBITDA — and EBITDA shapes exit multiples. That math makes spend management one of the most consequential levers in any operating partner's toolkit.

Most investment theses mention cost discipline. The gap between mentioning it and actually executing it — consistently, across multiple portfolio companies, over a multi-year hold — is where value leaks away.

A missed contract renewal here, an uncontracted vendor there, fragmented spend data across three ERP systems: none of it looks catastrophic in isolation. Together, it compounds into real EBITDA erosion.

Treating spend management as a back-office function is a choice — one that shows up at exit.

Key Takeaways

- Spend management in PE is the disciplined oversight of third-party and operational expenditures across portfolio companies to protect and grow EBITDA.

- Third-party spend typically represents 30–60% of revenue in PE-backed companies — making it the highest-impact cost category available.

- Done well, it delivers three measurable outcomes: EBITDA improvement, portfolio-wide spend visibility, and tighter risk and compliance control.

- Ignoring it creates compounding problems — maverick spending, contract auto-renewals, and fragmented data that erodes value creation momentum.

- Firms that embed spend management early and sustain it through the hold period exit with stronger EBITDA multiples and a cleaner value creation narrative.

What Is Spend Management in Private Equity?

Spend management is the structured process of analyzing, controlling, and optimizing how an organization allocates expenditures across categories — from direct procurement and vendor contracts to IT, professional services, and operational overhead. Unlike cost-cutting, which is a one-time event, spend management is an ongoing discipline that converts operational data into measurable financial outcomes.

In a PE context, it operates at two distinct levels:

- Portfolio company level: CFOs and procurement teams manage day-to-day spend, vendor contracts, and category optimization — with a focus on invoice accuracy and compliance

- Fund level: Operating partners run spend programs across the portfolio to identify cross-portfolio savings, benchmark performance, and drive consistent value creation

The problems at each level are distinct. A portfolio company CFO worries about invoice accuracy and contract compliance. An operating partner worries about whether the same vendor problem showing up at three different portfolio companies is being addressed systematically or handled in isolation three separate times.

Spend management connects both levels — giving operating partners the cross-portfolio visibility they need while giving portfolio CFOs the operational controls to act on it.

Key Advantages of Spend Management for PE Firms

Each advantage below is trackable through KPIs that PE stakeholders actually use: EBITDA margin, cost-to-revenue ratio, savings rate, and compliance posture.

EBITDA Improvement Through Third-Party Cost Optimization

Third-party spend — covering suppliers, service providers, and vendors — typically represents 30–60% of revenue in PE-backed companies, according to Efficio. For a mid-market portfolio company generating $100M in revenue, that's $30–60M of addressable cost sitting in vendor relationships, contracts, and procurement decisions.

Even modest savings rates have outsized impact. Efficio's PE portfolio-company model illustrates the math clearly: a company with €200M in annual spend, addressing 50% of that spend and achieving 8–12% savings, generates €8–12M in EBITDA improvement — which translates to €80–120M in enterprise value at a 10x multiple.

Spend management creates this outcome through a sequence of specific activities:

- Spend mapping — categorizing all expenditures to identify where money actually goes

- Market benchmarking — comparing vendor rates against what comparable companies pay

- Contract leakage identification — surfacing spend that falls outside negotiated terms

- Structured renegotiation — using data to create leverage with vendors who otherwise face no pressure to improve terms

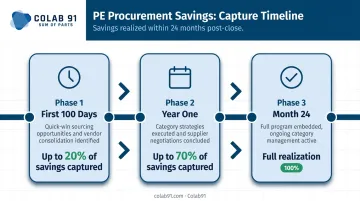

This is a distinctly PE advantage. Alvarez & Marsal reports that procurement savings in PE portfolio companies can be realized within 24 months post-close, with up to 70% captured in year one and up to 20% in the first 100 days. That front-loading aligns directly with how PE firms generate value — concentrated, measurable impact within the hold period rather than gradual gains that arrive too late to affect exit multiples.

KPIs impacted: EBITDA margin, savings rate as a percentage of addressable spend, cost-to-revenue ratio, contract compliance rate

When it matters most: Post-acquisition 100-day plans, add-on acquisition integration, and pre-exit EBITDA normalization

Portfolio-Wide Visibility and Financial Control

A PE firm managing multiple portfolio companies faces a visibility problem that individual company CFOs don't. Spend data sits in different ERP systems, accounting platforms, and reporting formats.

Operating partners trying to identify cross-portfolio patterns — or benchmark one company's cost structure against another's — are often working from incomplete, inconsistent information. Without a unified view, a software vendor overcharging one portfolio company may be doing the same at two others, and no one connects the dots.

Structured spend management addresses this by:

- Establishing consistent spend taxonomies across the portfolio

- Centralizing data into a unified view that supports both company-level and fund-level analysis

- Enabling cross-portfolio vendor leverage — renegotiating IT, SaaS, telecom, and professional services as a consolidated portfolio rather than company by company

The financial control benefits extend to LP reporting. When spend data is accurate, categorized consistently, and tracked in real time, accruals are cleaner, budget variance analysis is faster, and the numbers in quarterly LP packages hold up to scrutiny.

Ardent Partners' 2025 research found that best-in-class procurement teams have 91.7% of spend under management, compared to 61.1% for average performers. That 30-point gap translates directly into financial control — and into the quality of data available when it matters most.

KPIs impacted: Budget variance rate, spend-under-management percentage, accrual accuracy, time to close monthly financials

When it matters most: Firms managing three or more portfolio companies simultaneously, during add-on integration, and when preparing LP reporting packages

Risk Mitigation, Compliance, and LP Confidence

Spend management reduces financial and regulatory risk across several dimensions that PE firms can't afford to ignore.

On the regulatory side, the SEC's examination priorities have consistently emphasized accurate calculation and allocation of private fund fees and expenses. In 2022, the SEC charged Energy Capital Partners Management for failing to disclose disproportionate expense allocations, resulting in a $1M penalty and $3.3M in fund repayments.

That case illustrates what poor expense tracking costs a firm: direct financial penalties, required repayments, and reputational damage arriving precisely when a fund may be raising its next vehicle.

On the operational side, spend management reduces exposure through:

- Approval workflows that prevent unauthorized spending before it occurs

- Clean vendor records that reduce duplicate payments and billing errors

- Contract coverage tracking that flags auto-renewals and off-contract spend before they compound

- Audit trails that satisfy LP scrutiny and SEC examination

LP confidence now tracks directly with procurement maturity. ILPA's Standardized Due Diligence Questionnaire explicitly covers expenses, costs, service providers, and fund operations — meaning LPs are asking these questions directly. PE firms that can demonstrate structured spend oversight differentiate themselves during fundraising and reduce friction in operational due diligence reviews.

KPIs impacted: Compliance incident rate, percentage of spend under contract, invoice error rate, audit findings

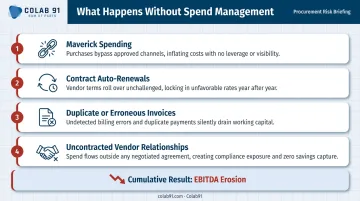

What Happens When Spend Management Is Ignored

Spend management failures don't announce themselves. They compound quietly — in duplicate invoices, missed renewal windows, and vendor relationships that were never put under contract in the first place.

Without structured spend management, portfolio companies typically experience:

- Maverick spending that bypasses approved vendors and negotiated rates, often without any visibility at the center

- Contract auto-renewals at unfavorable terms, often for services that haven't been benchmarked in years

- Duplicate or erroneous invoices that go undetected because no one owns the review process

- Uncontracted vendor relationships that create compliance exposure and unpredictable pricing

Consider a vendor billing a portfolio company $250K annually for a service originally contracted at $200K. Without a spend oversight function tracking contract terms against actual invoices, that discrepancy may not surface until an audit — by which point it's compounded across multiple billing cycles.

That gap isn't unusual. Recovery audit firms have built entire practices around finding exactly this type of contract leakage.

Multiply that across five or six portfolio companies and the problem stops being manageable. Operating partners lose the ability to distinguish genuine financial performance from cost concealment — and that uncertainty erodes confidence in the numbers they're presenting to LPs.

That LP credibility problem has a direct exit consequence. When a potential acquirer conducts buy-side due diligence on a company with uncontracted vendor relationships, inconsistent cost categorization, and unreliable EBITDA normalization, they have two options: reduce the valuation to account for the uncertainty, or walk away. Neither is acceptable after a multi-year hold.

How to Get the Most Value from Spend Management

Spend management delivers compounding returns when applied consistently across the hold period — not just at entry. Three practices separate firms that capture durable savings from those that see one-time results:

Establish a spend baseline within the first 90 days post-acquisition — identify the highest-impact cost categories before operational momentum pulls attention elsewhere. This baseline becomes the foundation for every savings initiative that follows.

Review spend performance on a regular cadence — monthly or quarterly, with clear ownership at the CFO and category-manager level. Savings initiatives that lack a review cadence tend to stall after initial momentum fades.

Treat spend data as a strategic input — not just a reporting output. Vendor consolidation decisions, contract renegotiation timing, and operating model changes should all be informed by what the spend data is showing.

The talent challenge is real. Building effective spend management capabilities requires expertise in strategic sourcing, spend analytics, and vendor management — skills that most mid-market portfolio companies don't have in-house and that take months to hire for.

Colab91 addresses this directly. The firm builds dedicated India-based procurement and analytics teams for PE-backed portfolio companies — pairing strategic sourcing expertise with an AI-powered spend analytics platform that ingests and classifies spend data across disparate ERP systems. Key capabilities include:

- Savings Opportunity Assessment completed in 4–6 weeks, typically identifying 5–15% of addressable spend as actionable savings with a category-by-category roadmap

- Cross-portfolio category leverage for PE operating partners, enabling contract renegotiation across IT, SaaS, telecom, and professional services at the portfolio level — not company by company

- Ongoing category management with clear ownership and savings tracking built in from day one

Done right, spend management becomes a repeatable capability — one that generates annual savings, improves forecast accuracy, and builds the financial discipline that future buyers and LP auditors expect to see.

Conclusion

Spend management is one of the most controllable and highest-return levers available to PE firms. It operates across the full hold period — improving EBITDA, reducing operational and compliance risk, and building a financial narrative that holds up at exit. Applied consistently, it produces compounding returns: cleaner data at exit, fewer compliance surprises mid-hold, and a cost structure that reflects deliberate decisions rather than accumulated drift.

Firms that achieve the best outcomes treat spend management as infrastructure, not intervention. They embed it early post-acquisition, maintain oversight through clear ownership and review cadences, and act on what the data surfaces. That structural approach — rather than a reactive cleanup before exit — is what converts procurement data into realized multiple expansion.

Colab91 helps PE sponsors and their portfolio companies build the offshore procurement and analytics teams that make this kind of continuous oversight practical. From spend analytics to category management and savings tracking, the capability is designed to operate across the hold period, not just at acquisition or exit.

Frequently Asked Questions

What is spend management in the context of private equity?

Spend management in PE is the structured oversight and optimization of expenditures across portfolio companies and at the fund level. The goal is improving EBITDA, reducing financial risk, and creating measurable value within the investment hold period — not just controlling costs in isolation.

How does spend management directly impact exit valuations?

EBITDA improvements driven by cost optimization flow directly through to deal valuations via exit multiples. Every dollar saved at the portfolio company level can generate several dollars of enterprise value, making procurement-led savings one of the highest-leverage tools available to operating partners.

What are the most common spend management challenges for PE-backed companies?

The most frequent problems include fragmented spend data across ERP systems, lack of in-house procurement expertise, and maverick spending outside approved vendors. Maintaining consistent cost discipline across portfolio companies with different accounting platforms compounds all three.

How is spend management different at the fund level versus the portfolio company level?

At the portfolio company level, spend management covers vendor contracts, procurement processes, and day-to-day operational costs. At the fund level, it shifts to benchmarking cost structures across the portfolio and ensuring management company expenses comply with LP agreements and SEC requirements.

When should PE firms start spend management initiatives — before or after acquisition?

The highest-impact window is the first 90–100 days post-acquisition — when a spend baseline can be established and quick wins identified. Pre-acquisition diligence should flag major spend risks early enough to shape the investment thesis and 100-day plan.

Do mid-market PE firms need dedicated procurement teams to manage spend effectively?

Not necessarily in-house. Mid-market PE firms and their portfolio companies often work with specialized offshore teams — like Colab91 — to access strategic sourcing and spend analytics expertise without building full internal procurement functions from scratch.