Introduction

Healthcare procurement is under pressure from every direction at once. Supply expenses per patient jumped 18.5% from 2019 to 2022, outpacing general inflation by nearly 30%, according to the American Hospital Association. Medical supplies now represent roughly 10.5% of the average hospital's operating budget - and that figure climbed another $6.6 billion between 2022 and 2023 alone.

At the same time, PE sponsors are demanding faster EBITDA improvement, regulators are tightening oversight, and supply chain shocks that once felt anomalous now arrive on a near-annual basis.

The organizations still running procurement on legacy assumptions - stable supplier relationships, predictable SKU counts, manageable regulatory load - are finding those assumptions increasingly expensive. Every month spent without addressing these gaps compounds the cost of catching up.

This guide covers the forces reshaping healthcare procurement over the next five years, the strategic pillars every organization must build, and a practical path to closing the capability gap.

TLDR

- Medical supply costs are rising faster than inflation and now consume ~10.5% of hospital budgets

- AI, value-based sourcing, and supply regionalization are rewriting the procurement playbook

- Five pillars define future-proof procurement: strategic sourcing, spend visibility, compliance, technology, and clinical alignment

- The talent gap is real; a blended onshore-offshore model is emerging as the practical solution

- Start with a spend diagnostic before investing in platforms or headcount

Why Current Healthcare Procurement Strategies Are Falling Short

Most healthcare procurement functions were designed for a different environment: a handful of trusted suppliers, predictable demand cycles, and enough budget buffer to absorb occasional inefficiencies. That structural assumption no longer holds.

COVID-19 exposed what was already broken. When the VA needed PPE at scale, antiquated inventory systems made the situation worse and some vendors failed to deliver entirely - the system ultimately obligated more than $4 billion for COVID-related products and services by May 2021.

The VA is a large, well-resourced system. Mid-market providers had even less margin for error.

The Operational Deficiencies Holding Teams Back

The gaps look similar across organizations:

- Fragmented spend data - purchases tracked separately across facilities, departments, and ERPs, with no consolidated view

- Limited sourcing coverage - procurement teams reactive rather than proactive, managing POs rather than categories

- Weak supplier visibility - no systematic monitoring of supplier financial health, delivery performance, or concentration risk

- Manual workflows - approval chains, contract tracking, and spend reporting still dependent on spreadsheets and email threads

Mid-market and PE-backed healthcare organizations growing through acquisition inherit all of these gaps simultaneously - often without the procurement infrastructure to consolidate them.

The EBITDA Consequence

HFMA research estimates that healthcare organizations pay 7% to 12% more than other industries for comparable nonclinical goods and services. Non-clinical spending alone can represent up to 30% of a health system's total spend. For a mid-market provider generating $200M in revenue, that gap translates to roughly $4M–$7M in excess annual spend - recoverable margin that most organizations aren't tracking.

Key Trends Reshaping Healthcare Procurement in the Next Five Years

AI and Predictive Analytics

AI in healthcare procurement has moved past basic automation. Health systems like Cleveland Clinic are now using AI and automated workflows to strengthen supply chain operations - including GenAI applications for sourcing and procurement, according to AHRMM. Predictive analytics is being used to maintain supply continuity during disruptions such as natural disasters, moving organizations from reactive firefighting to proactive planning.

Organizations that build these capabilities early gain a structural advantage across three areas:

- Better demand forecasting before shortages materialize

- Real-time supplier risk scoring instead of periodic reviews

- Spend analysis that runs continuously, not just quarterly

Value-Based Procurement

The shift from unit-cost purchasing to total cost of ownership (TCO) is accelerating - and the physician preference item (PPI) category illustrates why it matters. PPIs represent just 3% of purchase orders but 20% of total supply-chain spend, with pricing variation that defies logic. HFMA documents pedicle screw pricing ranging from $500 to $3,000 per unit for clinically comparable products.

The implication: procurement teams that evaluate only invoice price leave the most significant savings category largely untouched. Value analysis committees that incorporate clinical outcome data alongside cost benchmarks are closing that gap.

Supply Chain Regionalization and Dual-Sourcing

Single-source and single-country dependencies are a documented liability. The scale of that exposure is clear in the data:

- 48% of API Drug Master Files originated from India and 13% from China in 2021 (HHS ASPE)

- The US imports roughly 80% of active pharmaceutical ingredients

- The AHA recorded an average of 301 drugs in shortage per quarter during 2023

Procurement teams are now being asked to map supplier networks with resilience as a design criterion - building tiered supplier panels with primary, secondary, and emergency sourcing options for critical categories.

ESG and Ethical Sourcing

Sustainable procurement spending exceeded $939.7 million in 2022 across 370 hospitals reporting to Practice Greenhealth - with 68% holding formal sustainable procurement policies and 53% operating against established goals. PE sponsors and health system boards are now embedding ESG criteria directly into vendor qualification frameworks, covering supplier labor practices, emissions profiles, and supply base diversity.

Digital Procurement Platforms

Legacy systems leave spend data siloed by facility, contract compliance invisible between reviews, and category benchmarking dependent on manual pulls. Cloud-based source-to-contract and spend analytics platforms close these gaps:

- Consolidated spend visibility across all facilities in one view

- Real-time contract compliance tracking instead of periodic audits

- Category-level benchmarking that reveals enterprise-wide pricing leverage

For multi-site providers, that consolidated view is often the difference between capturing group-level pricing and leaving savings fragmented across locations.

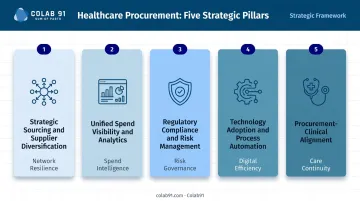

Five Pillars of a Future-Proof Healthcare Procurement Strategy

Pillar 1: Strategic Sourcing and Supplier Diversification

Future-proof procurement requires moving from transactional buying to proactive market analysis. That means:

- Regular supplier market assessments by category, not just at contract renewal

- Competitive sourcing events with documented award criteria and supplier scorecards

- Tiered supplier panels - primary, secondary, and spot vendors - for critical categories

- Concentration risk monitoring to identify over-reliance on single suppliers or geographies

The goal is removing single points of failure before a disruption forces the issue.

Pillar 2: Unified Spend Visibility and Analytics

Without a single view of what's being bought, from whom, at what price, and against which contract, every strategic decision is a guess. Unified spend visibility requires both a data infrastructure investment - normalizing spend across facilities and ERPs - and the analytical capability to act on it.

The analytical layer should be able to:

- Identify maverick spend and contract leakage

- Benchmark supplier pricing against market rates

- Flag categories with high spend concentration or limited sourcing coverage

- Prioritize where strategic sourcing investment will have the highest return

Pillar 3: Regulatory Compliance and Risk Management

114 Class I medical device recalls were recorded in 2024 - the highest since at least 2012. FDA 21 CFR 820.50 requires documented supplier evaluation processes. HIPAA mandates business associate agreements for data-sharing vendors. The compliance environment is demanding, and the stakes keep rising.

Treating compliance as a downstream audit activity - something checked after a supplier is already embedded - creates real exposure. Future-proof organizations build compliance into the sourcing workflow from the start:

- Supplier qualification criteria defined before award

- Ongoing audit schedules (not one-time reviews)

- Financial health monitoring for critical suppliers

- Product safety certification tracking as a standing discipline

Pillar 4: Technology Adoption and Process Automation

E-procurement tools, automated PO workflows, and contract management platforms eliminate administrative bottlenecks and reduce cost-to-procure. The goal isn't technology adoption for its own sake - it's freeing procurement professionals to focus on work that requires judgment:

- Supplier negotiations

- Category strategy development

- Clinical stakeholder engagement

- Market intelligence and benchmarking

When analysts spend their days chasing approval signatures and reconciling purchase orders, they're not doing any of that higher-value work.

Pillar 5: Procurement-Clinical Alignment

Procurement decisions made without clinical input create predictable problems: PPI proliferation, maverick buying, and product selections that optimize for price while missing clinical outcomes. PPIs - where physician preference carries enormous cost consequence - are the sharpest example of what misalignment costs.

Future-proof organizations embed value analysis committees (VACs) and cross-functional governance into their procurement operating model. This creates a structured process for evaluating new products on both clinical performance and total cost, reducing ad hoc purchasing decisions and building clinician trust in the procurement function.

Closing the Procurement Capability Gap: People, Data, and Domain Expertise

The Talent Problem

AHRMM survey data indicates that 55% of hospital purchasing leaders cite personnel shortages as a significant challenge. Healthcare procurement teams are frequently under-resourced relative to the spend they manage - and HFMA recommends allocating 0.6% to 0.8% of nonclinical spending to managing the procurement function, a benchmark most organizations fall short of.

The gap is sharpest in mid-market and PE-backed healthcare companies growing through acquisition. Each new entity adds spend complexity, supplier relationships, and compliance obligations that an already-stretched team absorbs without proportional headcount growth.

Build vs. Buy vs. Partner

Three paths exist, each with real trade-offs:

| Approach | Upside | Downside |

|---|---|---|

| Build fully in-house | Institutional knowledge, strategic control | Capital-intensive, slow to scale |

| Full outsourcing | Cost reduction | Loses strategic ownership, context |

| Blended capability model | Cost efficiency + strategic control | Requires deliberate design |

The blended model - a lean onshore team owning strategy, clinical relationships, and governance, supported by an offshore team handling spend analytics, market research, supplier benchmarking, and RFx execution - is emerging as the practical answer for mid-market organizations.

What Good Offshore Healthcare Procurement Support Looks Like

A dedicated capability center and a generic offshore staffing arrangement are not the same thing - and the difference matters more in healthcare than in most sectors. Healthcare procurement requires practitioners who understand:

- Clinical supply categories and their compliance constraints

- GPO contract structures and utilization dynamics

- The stakeholder complexity of clinical environments

- Regulatory obligations that vary by care setting

Colab91 has built and operated this model for healthcare clients including Pediatric Associates and Kindred Healthcare. Their advisory team includes Erika Jung, who served as CPO at Pediatric Associates (a TPG portfolio company) and has led enterprise-wide procurement transformation for PE-backed providers.

The Colab91 leadership team previously scaled Impendi's India operations to 100+ practitioners serving PE sponsors including Carlyle Group, TPG, Elliott, and BC Partners before the firm was acquired by Accenture. That combination of offshore delivery infrastructure and genuine healthcare domain expertise is what distinguishes a strategic partner from a headcount supplier.

Anchoring Capability Investment to Unified Spend Data

Any capability investment - people, tools, or partners - must be anchored to a unified, durable spend data foundation. Without it, analysts can't deliver consistent insights. Colab91's AI-powered spend analytics platform is designed specifically to create this layer: normalizing data across facilities, flagging contract leakage, and enabling category-level benchmarking that drives actual sourcing decisions.

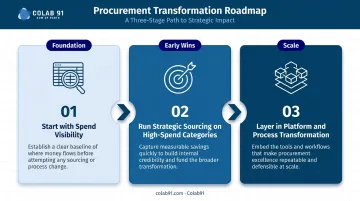

How to Get Started: A Practical Roadmap

Step 1: Assess Before You Invest

Before committing budget to platforms, headcount, or partners, conduct a current-state diagnostic that maps:

- Spend data quality and coverage by category

- Supplier concentration risk and single-source dependencies

- Sourcing coverage (what percentage of spend is under active category management)

- Compliance gaps in vendor qualification and contract management

- Team capacity relative to managed spend

This baseline tells you where to act first - and keeps you from sequencing investments in the wrong order.

Step 2: Sequence by Impact and Feasibility

Sequence investments by what unlocks the most value, fastest:

- Start with spend visibility. Without clean data, every downstream decision - sourcing targets, supplier negotiations, risk prioritization - is a guess.

- Run strategic sourcing on your highest-spend or highest-risk categories next. This generates early wins and builds internal capability before you tackle broader transformation.

- Layer in platform and process transformation last, when the data foundation is solid and the team has the sourcing muscle to use the tools effectively.

Step 3: Build for Scalability, Not Just Today

A future-proof procurement strategy must anticipate growth: acquisitions, new service lines, expanded facilities. That means designing governance structures, data standards, and operating models that scale without requiring a rebuild.

Concretely, scalability looks like:

- Documented category strategies that transfer across entities

- Supplier performance standards applied consistently

- Sourcing playbooks that new team members or offshore analysts can execute without tribal knowledge

- Data architecture designed for your 5-year footprint, not just your current state

Frequently Asked Questions

What does "future-proofing" actually mean in healthcare procurement?

Future-proofing means building procurement strategies, processes, and capabilities that remain effective despite disruptions - supply chain shocks, regulatory shifts, cost pressures, or organizational growth. The goal is resilience, not just optimization for current conditions.

What are the biggest supply chain risks healthcare procurement teams face today?

Single-source supplier dependencies, geopolitical concentration in pharmaceutical APIs, drug shortages (averaging 301 per quarter in 2023), and inflation in medical devices and specialty categories. Demographic shifts and disease-driven demand volatility add further unpredictability.

How does spend analytics improve healthcare procurement outcomes?

Spend analytics creates the visibility needed to identify savings opportunities, monitor contract compliance, benchmark supplier pricing, and prioritize which categories deserve strategic sourcing investment - moving teams from firefighting to deliberate category strategy.

What is value-based procurement and how is it different from cost-focused buying?

Value-based procurement evaluates total cost of ownership and clinical outcomes alongside purchase price. A slightly higher-cost product that reduces complications or readmissions may deliver greater value than the cheapest option alone.

How should PE-backed healthcare companies approach procurement transformation?

PE-backed organizations face real-time pressure. Prioritize rapid spend visibility, quick-win sourcing initiatives in high-spend categories, and scalable operating models that support both near-term EBITDA improvement and platform company growth across a growing portfolio.

When does it make sense to use an offshore procurement team versus building in-house?

Offshore is most effective for analytics-heavy, high-volume, or repeatable work: spend analysis, market research, RFx support, supplier benchmarking. Onshore resources should remain focused on clinical stakeholder relationships, strategic negotiation, and governance. The blended model captures cost efficiency without sacrificing strategic control.