Introduction

Finance and procurement teams at mid-market and PE-backed companies often know money has gone out - they just can't say with confidence how much is unreconciled, where it sits, or what risk it carries. Budget decisions get made on data that's weeks old, and no one finds out until the damage is done.

Most organizations have the raw data. What they lack is a continuous, connected view of it. According to a 2024 BlackLine survey of over 1,300 senior finance professionals, nearly 40% of CFOs don't completely trust their organization's financial data, and 31% cite too many disparate sources as the primary reason.

This guide walks through the data sources, methods, and oversight practices needed to move from periodic reconciliation snapshots to a continuously updated view of unreconciled spend - including how to act when that visibility surfaces a problem.

Key Takeaways

- Unreconciled spend is any expenditure committed, accrued, or processed that hasn't been confirmed across POs, invoices, and ledger records

- Root causes include disconnected systems, batch-cycle reconciliation, and weak three-way match discipline

- Three methods exist: manual report reviews, ERP-integrated automated matching, and a dedicated spend analytics layer

- Real-time visibility helps teams classify spend as pending, at risk, or a control gap - and act accordingly

- Sustained visibility requires ongoing process discipline - not just a one-time data cleanup

What You Need to Monitor Unreconciled Spend in Real Time

Real-time visibility into unreconciled spend starts with confirming the right data sources are connected and baseline records are structured consistently enough to match against.

Data Sources and Systems Required

Real-time monitoring requires four data inputs, all drawing from a common or connected data layer:

- Purchase order data from your procurement system

- Invoice records from accounts payable

- Payment confirmations from banking or treasury feeds

- Contract and commitment data for accrual comparison

Most mid-market organizations don't have these sources in one place. APQC benchmarks show that finance shared services organizations run a median of 3.0 ERP instances across their environment.

Fragmented source systems - separate ERP modules, offline spreadsheets, disconnected procurement tools - must be mapped before any visibility method produces reliable output.

Preconditions and Baseline Setup

Two setup conditions determine whether automated matching holds up:

Consistent reference data - PO numbering conventions, vendor master records, and cost center codes must align across entities. Mismatched reference data is one of the most common reasons automated matching fails and unreconciled items accumulate.

**Defined ownership per spend category** - establish a reconciliation period and a clear accountable party for each entity or category. When unreconciled items surface, someone specific needs to be working toward resolution - not an open shared queue with no clear owner.

Why Unreconciled Spend Accumulates

Reconciliation backlogs in mid-market and PE-backed environments aren't usually caused by individual errors. They're produced by structural patterns that reliably create the same problems at scale.

Batch-cycle reconciliation is the most pervasive cause. When matching only runs monthly or quarterly, spend committed in week one remains unconfirmed until the cycle closes - a live cash commitment with no visibility layer over it for weeks.

Three-way match failures create persistent unreconciled items. When a purchase order, goods receipt, and invoice don't align on quantity, price, or vendor reference, the invoice stalls in an approval queue rather than posting. According to Ardent Partners' 2024 State of ePayables report - based on a survey of 212 AP and finance professionals - the average invoice exception rate is 14%, rising to 22% for organizations outside Best-in-Class. That's a large volume of committed spend stuck in approval queues at any given moment.

Three more structural causes compound the backlog:

- Maverick spend - purchases made outside approved channels without a PO - enters the ledger at invoice or payment stage with nothing to match against. It's structurally unreconcilable under standard matching rules and invisible until someone investigates manually. The same Ardent Partners report found that only 61% of invoices are linked to a purchase order on average, versus 83.7% for Best-in-Class operations.

- Multi-entity complexity adds surface area in PE-backed portfolios. Intercompany recharges, shared service allocations, and currency-adjusted accruals each require separate reconciliation before rolling into a consolidated spend position.

- Accrual mismatches surface when a period-end accrual for uninvoiced spend is later settled by an invoice at a different amount or in a different period. The reversal doesn't automatically clear the original entry, leaving a ghost balance that ages silently across reporting periods.

Methods to Build Real-Time Visibility Into Unreconciled Spend

Three distinct approaches exist, ranging from labor-intensive to always-on. The right choice depends on transaction volume, system maturity, and available finance team resources.

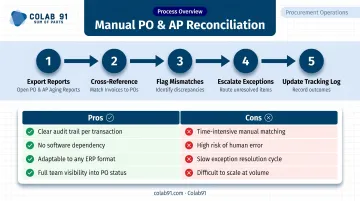

Method 1: Manual Ledger and Report Reviews

What it is: Finance team members pull periodic reports from the ERP - typically AP aging, open PO reports, and unapplied cash listings - and manually identify items that haven't cleared or matched. This is the current default for most mid-market teams without dedicated reconciliation tooling.

How it works:

- Export the open PO report and AP aging from the ERP

- Cross-reference invoices against POs using shared vendor and reference identifiers

- Flag items where invoice amount, date, or vendor doesn't match the originating PO

- Escalate exceptions to procurement or AP for resolution

- Update the tracking log before the next review cycle

Trade-offs:

| Pros | Cons |

|---|---|

| Low setup cost, works with any ERP | Point-in-time snapshot only |

| No new tooling required | Highly dependent on individual effort |

| Flexible and adaptable | Typically surfaces issues weeks after they occur |

Method 2: ERP-Integrated Automated Matching

What it is: Automated matching rules within the ERP or a connected reconciliation tool compare incoming invoices against open POs in real time, flagging exceptions immediately rather than waiting for a manual review cycle.

How it works:

- Configure matching tolerance thresholds (acceptable price or quantity variance) within the ERP procurement module

- Set automated routing rules so exceptions go to a named queue - not a silent stall

- Schedule daily or intraday reconciliation runs to update the unreconciled spend register

- Use exception dashboards to review only items that failed automated matching

- Track exception resolution time as an operational KPI

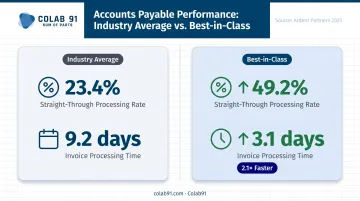

The performance gap between automated and manual approaches is significant. Ardent Partners' 2025 AP Metrics report found that Best-in-Class organizations achieve 49.2% straight-through invoice processing compared to 23.4% for everyone else - and process invoices in 3.1 days versus the 9.2-day average.

Those numbers make the case for investment. Trade-offs: Significantly reduces reconciliation lag; requires upfront configuration and ongoing rule maintenance. Works best when vendor master data, PO references, and cost codes are clean and consistent.

Method 3: Dedicated Spend Analytics Function with a Unified Data Layer

What it is: A purpose-built spend analytics function - combining human analysts with an AI-powered unified data layer - continuously monitors spend across procurement, AP, and banking feeds. It classifies transactions, flags anomalies, and maintains a live register of unreconciled items across categories and entities. PE-backed companies managing spend across 3–10 acquired entities are the primary use case.

How it works:

- Build or deploy a unified spend data layer that ingests PO, invoice, payment, and contract data from all source systems on a defined refresh schedule

- Apply AI-assisted categorization and matching logic to auto-classify transactions and surface mismatches

- Assign offshore spend analysts to manage daily exception triage and resolution

- Produce a live unreconciled spend dashboard accessible to CFO, Controller, and procurement leadership

- Set alert thresholds for high-value or aging unreconciled items

This is the model Colab91 builds for mid-market and PE-backed clients - pairing offshore spend analysts with AI-powered spend analytics tools to create a visibility function that runs continuously. The offshore delivery model keeps costs manageable without requiring full onshore headcount.

Trade-offs: Provides the most complete and current view; scales across entities; turns reconciliation from a manual burden into a continuous finance function. Requires investment in data infrastructure and analyst capacity - offset by offshore delivery economics.

How to Read and Act on Your Unreconciled Spend Data

A real-time unreconciled spend view only pays off when you know what each category of exception means - and what it demands from you. Here's how to read the signals.

Normal / Acceptable State

A healthy unreconciled spend register shows a small, stable volume of items in early-stage matching - recently submitted invoices not yet through the three-way match cycle, aging well within the standard processing window, concentrated in known high-volume categories. This is normal pipeline, not a control issue.

Next step: Routine monitoring only.

Warning Signs

The following patterns require investigation:

- Unreconciled items aging beyond the standard processing window

- A growing volume of partial-match exceptions where invoices and POs share a vendor but differ on amount or reference

- A concentration of unreconciled spend in a single cost center or vendor

These often signal a process breakdown, a vendor billing pattern change, or a data quality issue in the PO system.

Next step: Escalate to the relevant category owner or AP lead for targeted review within 48 hours.

Critical / Action-Required State

These are control gaps, not timing issues:

- Unreconciled items with no corresponding PO (potential maverick spend)

- Duplicate invoices in the unmatched queue

- Unreconciled balances persisting across more than one reporting period without resolution

- A sudden spike in total unreconciled value without a corresponding increase in approved spend

Next step: Freeze further payment on flagged vendors until resolution is confirmed. Initiate a root cause review and escalate to finance leadership.

The fraud exposure is real. The ACFE's 2024 Report to the Nations found that billing schemes appeared in 22% of occupational fraud cases, with a median loss of $100,000 - and 19% of fraudsters concealed their activity through altered account reconciliations.

Best Practices for Sustaining Real-Time Spend Visibility

Real-time visibility degrades fast when the processes behind it aren't maintained. Without consistent discipline around data quality, exception handling, and metric tracking, even a well-configured system drifts out of sync within weeks.

Daily exception review cadence. Assign a named owner to work through the unreconciled spend register each day, focusing only on exceptions that failed automated matching. This keeps the queue small, resolution timely, and the live spend view reflecting current reality rather than last week's backlog.

Track three operational metrics:

- Unreconciled spend as a percentage of total processed spend - a declining ratio reflects tighter matching discipline

- Average age of open exceptions in days - a shorter average signals faster resolution

- Share of transactions that auto-match without manual intervention - a rising share indicates improving data quality and matching rule performance

Clean master data outperforms any software upgrade. Vendor name normalization, consistent PO reference formatting, and aligned cost center coding across entities do more to improve matching accuracy than switching platforms.

APQC benchmarks show that top-performing organizations process 99% of invoices error-free the first time, compared to just 60% for bottom performers. That gap traces back almost entirely to data quality, not tool selection.

Frequently Asked Questions

What is unreconciled spend in procurement?

Unreconciled spend refers to any expenditure that has been committed, accrued, or invoiced but not yet confirmed through the matching process. No verified link exists between the purchase order, goods or services received, and the invoice or payment record - leaving a financial position on the books that hasn't been validated.

What are the risks of unreconciled accounts?

Key risks include:

- Overstated or understated liabilities on the balance sheet

- Inaccurate cash flow forecasting

- Duplicate payments and fraud exposure, including concealment through altered reconciliations

- Compliance risk when unreconciled balances persist into audit periods without documented resolution

Why is bank reconciliation not balancing?

The most common causes are timing differences between when transactions post in the ERP versus when they clear the bank, transactions posted to the wrong account or period, unapplied cash sitting in clearing accounts, and bank fees or errors not yet captured in the internal ledger.

What causes spend to go unreconciled?

The structural causes are three-way match failures where PO, receipt, and invoice don't align; maverick purchases made without a PO; accruals that don't reverse cleanly when the actual invoice arrives; and batch-cycle reconciliation processes that only run monthly rather than continuously.

How often should unreconciled spend be reviewed?

High-volume or PE-backed environments should aim for daily exception reviews. Simpler organizations can operate on a weekly cadence. The practical standard: no unreconciled item should age beyond the standard payment window without a named owner actively working toward resolution.

How do I get real-time spend visibility without replacing my ERP?

Real-time visibility doesn't require replacing the ERP. It requires connecting the data that already exists within it - through automated matching rules, structured exception workflows, and a unified spend data layer that refreshes daily rather than monthly.