Introduction

U.S. hospitals spent $146.9 billion on medical supplies in 2023, representing roughly 10.5% of the average hospital budget, according to the AHA's 2024 Costs of Caring report. Add purchased services - which HFMA estimates can represent as much as 30% of hospital nonlabor expense - and the non-labor cost base becomes one of the most consequential levers in any healthcare organization's financial profile.

For PE-backed providers and multi-site operators, this matters directly at the EBITDA line. Every dollar of unmanaged procurement cost compounds across facilities, contract cycles, and acquisition integrations.

These costs aren't fixed. They become expensive through fragmented decision-making, unmanaged clinical preferences, and weak contract governance - not because healthcare is inherently expensive to operate. This guide examines cost reduction across three dimensions:

- Better upfront decisions - GPO leverage, standardization, purchasing policy

- Tighter management - spend analytics, contract compliance, supplier accountability

- Structural changes - automation, portfolio aggregation, offshore capability

Key Takeaways

- Healthcare procurement costs accumulate through fragmented purchasing, physician preference item proliferation, and off-contract spend - gaps that only structured spend analysis reliably surfaces

- Medical supplies and purchased services together represent one of the largest non-labor cost categories in healthcare operations

- The highest-impact reduction levers span decisions, management practices, and structural investments - no single lever is sufficient alone

- Clinical stakeholder buy-in and procurement discipline must work together; either without the other produces short-lived results

- PE-backed and mid-market healthcare companies that build durable analytics and sourcing capability capture sustained value, not one-time savings

How Healthcare Procurement Costs Typically Build Up

Procurement cost rarely appears as a single, visible problem. It accumulates incrementally - through off-contract purchases, supplier base drift, and contracted price erosion that compounds across billing cycles and budget years.

The M&A Compounding Effect

Acquisition-driven growth makes this worse. When healthcare organizations add facilities through M&A, each site typically arrives with its own supplier relationships, negotiated pricing, and contract terms. The result: duplicative cost structures, missed volume consolidation opportunities, and pricing inconsistency for identical items across sites.

HFMA estimates that supply-chain integration after healthcare M&A can account for 3% to 8% in total cost savings - and roughly 50% of total deal synergy value. That's a significant proportion of transaction value sitting in procurement, often underactioned during integration.

Rogue Spend as a Hidden Leak

Maverick or rogue spend - purchasing that bypasses approved contracts - is a persistent cost leak that standard financial reporting rarely surfaces. Vizient benchmarks suggest that ideally 90% of healthcare supply chain transactions should be covered under contract, leaving organizations without active compliance monitoring significantly exposed on cost.

These costs stay hidden until scale or financial scrutiny forces a reckoning. What typically surfaces the gap:

- A PE sponsor's value creation review identifying procurement as an underperforming lever

- A CFO-driven cost initiative requiring category-level spend visibility

- A structured spend analysis program revealing contract compliance failures

By the time any of these triggers fires, the gap has usually been accumulating for years.

Key Cost Drivers in Healthcare Procurement

Understanding where cost originates determines which interventions actually work. Four drivers account for the majority of excess spend across healthcare organizations.

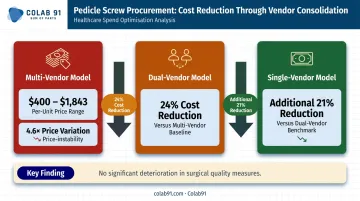

Clinical Preference Items

Physician preference items (PPIs) - implants, devices, and supplies selected based on individual physician preference rather than clinical evidence - represent 40% to 60% of hospital supply costs, according to peer-reviewed research. The procurement challenge is structural: purchasing decisions happen outside procurement's control, at the point of clinical choice.

A JAMA Network Open study of spinal implant procurement illustrates the magnitude. Pedicle screw prices ranged from $400 to $1,843 across vendors - a 4.6x price variation for the same item. Moving from a multi-vendor model to a dual-vendor model reduced commodity implant costs by 24%, with a single-vendor consolidation producing an additional 21% reduction. Surgical quality measures showed no significant deterioration.

Supply Chain Fragmentation

Each facility negotiating independently means:

- Volume is split across suppliers instead of consolidated

- Tier-based pricing thresholds go unmet

- The same item carries different prices across sites with no systematic correction

For multi-site operators, this fragmentation can be one of the most recoverable cost categories - because the fix is structural rather than clinical.

Contract Non-Compliance and Auto-Renewals

Off-contract purchasing, missed renewal windows, and auto-renewals on legacy terms create recoverable cost leakage. Procurement teams without active monitoring systems rarely catch this in time. Spend drifts off-contract quietly, and unfavorable terms roll over automatically before anyone flags them.

Common leakage points include:

- Off-contract purchases made by departments bypassing approved vendors

- Auto-renewals locking in legacy pricing without renegotiation

- Missed contract windows that forfeit earned rebates or volume discounts

Reactive, Manual Purchasing

Organizations relying on manual purchase orders, paper-based invoicing, and reactive reordering pay more than they should. Premier estimates that up to 70% of healthcare invoices are still managed through paper-based workflows - a process that generates matching errors, payment delays, and overbilling exposure across hundreds of transactions.

Cost-Reduction Strategies for Healthcare Procurement

Effective cost reduction must match the intervention to where cost originates. The strategies below are organized across three categories: changing procurement decisions, improving how procurement is managed, and addressing structural factors.

Strategies That Change Procurement Decisions

These approaches target the choices made before or around purchasing commitments - where leverage is highest and savings most durable.

GPO leverage and contract tier optimization

Approximately 96% to 98% of U.S. hospitals purchase through GPO contracts, with most using two to four GPOs per facility. But passive GPO membership and active tier management are very different things. Organizations that audit their tier qualifications and shift volume to reach better pricing thresholds unlock additional savings without renegotiating contracts from scratch. The gap between what organizations pay and what they could pay on their existing GPO agreements is frequently material.

Clinical preference item standardization

Value analysis committees (VACs) - cross-functional teams of clinicians, supply chain, and finance - evaluate new product requests and assess existing preference items against clinical outcome evidence. This is one of the highest-impact decisions a healthcare organization can make, because it addresses cost at the point of clinical choice rather than after the purchasing commitment is made.

Getting clinical buy-in is the hard part. The organizations that do it well treat VAC processes as clinical quality initiatives, not cost-cutting exercises - and they bring outcome data, not just price comparisons, to the table.

Consolidated purchasing policy across sites

Multi-site and PE-backed organizations that allow individual facilities to independently contract for categories already under enterprise agreements pay for the same capability twice. A coordinated purchasing policy that routes volume through enterprise agreements builds leverage for renegotiation while eliminating duplicative spend.

Formulary and product substitution discipline

Structured approval processes for new supply additions - requiring cost-outcome justification before an item enters the supply base - prevent silent preference item proliferation and protect standardization gains over time.

Strategies That Change How Procurement Is Managed

These approaches reduce cost by improving visibility, control, and consistency in day-to-day procurement operations.

Spend analytics and category management

Spend analytics is the prerequisite for almost every other cost reduction initiative. Without categorized, clean spend data, savings targets are guesswork. With it, they become defensible commitments tied to real numbers.

McKinsey estimates that structured spend optimization can deliver 5% to 15% cost savings on health systems' external spend. A functioning spend analytics capability surfaces:

- Off-contract purchasing by category and facility

- Price variation for identical items across sites

- Supplier concentration and fragmentation

- Contract coverage gaps and renewal risk

For Colab91's clients, this analytical foundation is typically what makes everything downstream - GPO tier analysis, category-level sourcing, supplier consolidation - actually executable rather than theoretical.

Contract compliance monitoring

Tracking whether actual purchasing behavior matches contracted commitments allows procurement teams to redirect off-contract spend and recover leakage before it compounds. Missed renewal windows and auto-renewals on unfavorable legacy contracts are a specific, recoverable cost category that most organizations can address within 90 days of establishing a monitoring function.

Supplier performance scorecards and reviews

Regular, cadenced supplier reviews with defined metrics - pricing compliance, fill rates, delivery accuracy - give procurement teams evidence for renegotiation and create accountability that prevents incremental price erosion. Without structured reviews, suppliers have little reason to hold pricing, and procurement teams have little leverage to enforce it.

Category-level sourcing strategies

Treating all procurement the same is a common mistake. The right approach differentiates by category:

- Commodity categories: competitive bidding

- Strategic suppliers: partnership and joint value modeling

- GPO-contracted items: compliance management and tier optimization

- Preference items: VAC-driven standardization

Strategies That Change the Structural Context Around Procurement

In many healthcare organizations, the operational setup itself is a primary cost driver - fragmented systems, manual processes, and procurement functions that lack the resources to manage spend actively.

E-procurement and workflow automation

Automated purchase order creation, invoice matching, and three-way matching (PO, receipt, invoice) recover overbilling and incorrect charges that manual processes miss. The operational evidence is clear: one large provider study found order discrepancies fell from 15% to 1.1% after moving the majority of purchase volume onto an automated platform. Premier data suggests 5% to 15% of invoices contain match-exception errors - errors that accumulate as real cost if not caught systematically.

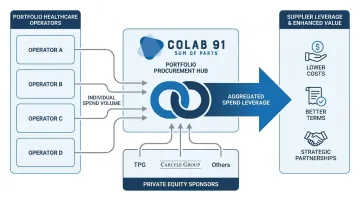

Spend aggregation for PE-backed portfolio companies

PE sponsors with multiple healthcare portfolio companies have a structural advantage that individual operators don't: the ability to aggregate spend across the portfolio. Categories like medical consumables, facilities management, IT services, and professional services all carry materially better pricing at portfolio scale than at individual company scale.

Portfolio-level engagement - as Colab91 has structured with sponsors including TPG and Carlyle Group - scales savings potential in proportion to aggregated volume rather than any single operator's purchasing power. When the engagement is designed from the outset at portfolio level, that structural advantage compounds across categories.

Building offshore procurement analytics and sourcing capability

One underused lever for mid-market and PE-backed healthcare organizations is offshoring the analytical and operational functions of procurement. The functions that benefit most include:

- Spend data management and cleansing

- Supplier research and RFP support

- Contract data extraction and tracking

- Savings opportunity identification and monitoring

This reduces the fully loaded cost of running a procurement analytics function while maintaining - or improving - output quality. The key distinction from consulting or staff augmentation is durability: a dedicated offshore capability center builds institutional knowledge, sustains analytics output between strategic initiatives, and scales as the organization grows.

Colab91 builds these offshore procurement and analytics centers for PE-backed and mid-market healthcare clients. For organizations like Pediatric Associates - a TPG portfolio company - the model delivers a durable capability rather than a time-limited engagement.

That design philosophy comes from direct experience: the Colab91 leadership team scaled Impendi's India operations (later acquired by Accenture) to 100+ practitioners serving clients including Carlyle Group and BC Partners, and that track record directly shapes how these centers are designed and delivered.

Strategic sourcing partnerships over transactional vendor relationships

Repositioning key supplier relationships from transactional to strategic shifts the basis of cost reduction from one-time negotiation to continuous, relationship-driven savings. Collaborative demand forecasting, joint cost modeling, and co-investment in process improvement all contribute to this. The approach matters most in categories where switching costs are high or where supplier expertise genuinely adds value beyond commodity pricing.

Conclusion

Reducing healthcare procurement costs depends on correctly diagnosing where cost originates - whether in clinical decisions, process breakdowns, contract non-compliance, or structural under-investment. Without that diagnosis, blunt cost-cutting pressure erodes supplier trust, clinical quality, and supply continuity.

The organizations that achieve durable results share three capabilities:

- Build analytics infrastructure that surfaces the true cost picture - not just headline spend

- Engage clinical stakeholders as partners in the process, not barriers to work around

- Resource procurement functions appropriately, including through offshore models that make sustained capability economically viable for mid-market operators

For PE-backed healthcare companies in particular, the difference between one-time savings and sustained value creation comes down to one question: does procurement capability outlast the initiative that created it?

Frequently Asked Questions

What are the five key needs that contribute to healthcare cost minimization strategies?

The five core needs are spend visibility, clinical stakeholder engagement, contract governance, supplier leverage (through GPOs or direct negotiation), and process efficiency. These work together rather than in isolation - spend visibility without contract governance, for example, surfaces problems without resolving them.

What are the 5 R's of procurement?

The 5 R's are Right quality, Right quantity, Right time, Right source, and Right price. In healthcare, quality and compliance carry additional stakes beyond typical commercial procurement - the wrong item at the right price can create clinical risk, not savings.

What is the biggest cost driver in healthcare procurement?

Clinical preference items (supplies chosen by physician preference rather than cost-outcome evidence) represent 40% to 60% of hospital supply costs in peer-reviewed research, making them the single largest controllable cost driver. They're also the hardest to address because the decision point sits outside procurement's direct control.

How do Group Purchasing Organizations reduce procurement costs in healthcare?

GPOs aggregate purchasing volume across member hospitals to negotiate discounted contracts, giving individual organizations access to pricing they couldn't achieve independently. That said, passive members consistently leave savings on the table - active tier compliance management is what separates high performers from average ones.

How can PE-backed healthcare companies accelerate procurement cost reduction?

PE sponsors accelerate savings by aggregating spend across portfolio companies, deploying dedicated procurement analytics resources quickly, and prioritizing high-impact categories first. Engaging at the portfolio level (rather than company by company) compounds leverage and compresses the timeline considerably.

What percentage of healthcare supply costs can strategic procurement reduce?

McKinsey estimates 5% to 15% savings on external spend; a Guidehouse analysis of 2,127 hospitals found an average opportunity of 17.4% of supply expense, or $12.1 million per hospital. Actual results vary based on organizational maturity, category mix, and whether cost avoidance is counted alongside direct reduction.