Introduction

PwC's Behind the Numbers report projects a 9% commercial medical cost trend for 2027—the highest in nearly two decades—with 2026 already restated at the same level. Aon corroborates this, projecting employer health costs will exceed $17,000 per employee in 2026, up from roughly $15,860 in 2025.

For healthcare providers and PE-backed healthcare organizations, sustained inflation at this rate doesn't just pressure budgets. It compresses operating margins, cuts into reinvestment capacity, and erodes the equity value that sponsors and operators have spent years building.

Here's what most organizations miss: healthcare costs aren't unmanageable by nature. They become expensive because of decisions made (or deferred) across procurement, operations, workforce, and care delivery. The organizations managing costs effectively in 2026 are making different choices upstream. Specifically, they're doing three things:

- Intervening earlier in procurement and contracting decisions

- Tightening operational controls that have historically gone unaudited

- Restructuring how administrative and analytical work gets resourced

This article examines where those costs originate—and which interventions are producing measurable results in 2026.

Key Takeaways

- Medical cost trend sits at 9% for 2026–2027, compressing margins across providers, employers, and PE-backed platforms simultaneously

- Pharmacy, labor, administrative overhead, and vendor fragmentation compound independently — and each becomes systemic before most organizations act

- Durable cost reduction spans three layers: upstream plan design, operational analytics and staffing controls, and structural changes to network and delivery models

- PE-backed healthcare organizations have the highest leverage in portfolio-wide spend consolidation and operational model redesign

- Cost reduction that sticks is a recurring management discipline, not a one-time budget exercise

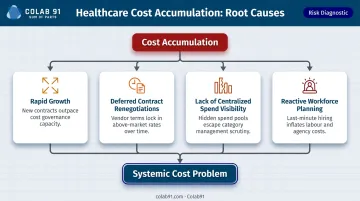

How Healthcare Costs Typically Build Up

Healthcare costs rarely announce themselves. They accumulate—across labor, pharmacy, supply chain, administrative functions, and third-party vendor relationships. Each category compounds independently, and by the time the problem surfaces on a balance sheet, it's already systemic.

The build-up is usually triggered by specific organizational conditions:

- Rapid growth through acquisition or expansion that outpaces procurement discipline

- Deferred contract renegotiations that allow vendor pricing to drift above market

- Lack of centralized spend visibility that lets duplicate contracts and off-contract purchases multiply

- Reactive workforce planning that resolves staffing gaps with contract labor rather than structural fixes

PE-backed healthcare companies undergoing portfolio integration face all of these simultaneously. Each acquired entity arrives with its own vendor relationships, staffing models, and administrative processes— rarely built for portfolio-wide efficiency.

Many of these costs stay hidden until scale or financial stress forces them into view. Duplicate supplier contracts, overbilling in revenue cycle functions, overtime patterns masking chronic understaffing — none of it registers until a financial review puts the compounding on the table.

Key Cost Drivers for Healthcare Organizations in 2026

Labor and Workforce Costs

Labor is the dominant expense for most healthcare organizations. According to the AHA's 2025 Cost of Caring Report, labor accounts for 56% of total hospital expenses, with total hospital expenses growing 5.1% in 2024—nearly double overall inflation.

The premium labor problem is particularly acute. A peer-reviewed 2026 nurse staffing cost study found contract nurses earning $112.60 per hour versus $56.24 for core staff—roughly a 100% premium. Contract labor expenses have reached as high as 258% of permanent staff costs in some systems.

The root issue isn't just wage rates. Staffing model misalignment with actual demand—scheduling that doesn't reflect patient volume and acuity—is what drives runaway labor costs. Agency over-reliance follows from that misalignment; it's a downstream consequence, not the origin of the problem.

Pharmacy and Specialty Drug Spend

Pharmacy has become one of the top-three cost inflators for employers and health plans. Business Group on Health data shows pharmacy represented 24% of employer total health care spend in 2024, with specialty pharmacy costs rising 14% over 2024 according to WTW.

GLP-1s are the flashpoint. Weight-loss GLP-1s are priced above $1,000 per month before rebates, and EBRI simulations suggest GLP-1 coverage could raise employment-based premiums by 5.3% to 13.8% depending on adherence assumptions. With 44% of employers with 500+ employees now covering GLP-1s for obesity, the cost exposure is no longer hypothetical.

Administrative Overhead and Billing Complexity

Administrative costs consume a disproportionate share of healthcare operating budgets—not because of care volume, but because of system fragmentation and manual processes.

Key benchmarks:

- Administrative expenses account for 15% to 25% of total U.S. health care spending (JAMA)

- The medical industry spent $83 billion annually on administrative tasks in 2022, with 97% attributed to provider transactions (CAQH)

- Physicians and staff spend an average of 13 hours per week on prior authorization alone (AMA)

- Median final denial rates rose from 2.5% in 2024 to 2.7% in 2025, while overturn success fell from 42.7% to 42.1% (Kodiak)

Each tenth-of-a-point increase in denial rates compounds across thousands of claims — and declining overturn success means less of that revenue is recoverable.

Supply Chain and Vendor Fragmentation

Healthcare providers manage an average of 1,200+ suppliers, according to GHX. At that fragmentation level, organizations lose purchasing leverage and contract visibility simultaneously—paying premium prices across dozens of uncoordinated relationships.

McKinsey benchmarks suggest health systems can realize **5% to 15% savings from external spend optimization**. Kaleida Health's partnership with Premier produced $75 million in savings from 2018 to 2023, including $17.7 million from data-driven value analysis alone.

Provider Reimbursement Pressure and AI Documentation Risk

Provider consolidation has steadily reduced payer negotiating leverage. The share of community hospitals affiliated with a system rose from 53% in 2005 to 68% in 2022, and a JAMA Health Forum study found primary care consolidation associated with a $14.55 (7.8%) increase in commercial prices per encounter.

Layered on top of consolidation pressure is a newer dynamic: ambient AI scribing tools are increasing billing and risk-adjustment coding intensity across provider settings. Early evidence from a 2025 PMC policy brief suggests this triggers payer responses including downcoding. For healthcare finance leaders, these tools represent a dual exposure — productivity gains on one side, revenue integrity risk on the other — and both sides need to be in the 2026 cost plan.

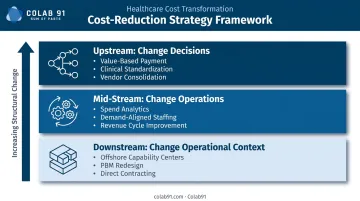

Cost-Reduction Strategies for Healthcare Organizations

Effective cost reduction depends on where costs originate. The strategies below are organized by the type of change required: changing decisions upstream, improving how operations are managed mid-stream, and restructuring the operational context downstream.

Strategies That Reduce Costs by Changing Decisions

These are upstream levers—most impactful when applied before cost pressures materialize.

Shift payment incentives toward value-based structures. Align reimbursement with outcomes rather than volume. Partner with centers of excellence for high-cost procedures, benchmark provider pricing, and steer plan members toward high-value providers through benefit design—not just benefit cuts.

Standardize clinical protocols to reduce unnecessary utilization. Evidence-based protocols that eliminate low-value treatments and redundant procedures deliver compounding savings over time. A clinical standardization initiative for hospital-acquired pressure injuries cited in PMC achieved a 63.2% reduction in HAPIs, avoided $438,000 in treatment costs, and eliminated 84 unnecessary length-of-stay days.

Consolidate vendor contracts and rationalize the supplier base. Reduce active vendors across non-clinical and clinical supply categories by consolidating contracts and increasing purchase volume per supplier. This is especially impactful for PE-backed organizations managing multiple acquired entities with duplicated supplier relationships—where cross-portfolio purchasing scale can extract pricing that no single entity could negotiate alone.

Strategies That Reduce Costs by Changing How Operations Are Managed

These improve visibility, consistency, and control over active operations without requiring structural redesign.

Deploy spend analytics and data-driven cost management. Organizations with centralized spend visibility can identify cost outliers, track contract compliance, and flag high-cost categories before they escalate. Colab91's spend analytics platform cleanses, classifies, and enriches healthcare spend data to surface savings opportunities across medical/surgical supplies, GPO contracts, purchased services, and contingent clinical labor.

The platform has been deployed with healthcare organizations including Pediatric Associates and Kindred Healthcare, giving procurement and finance teams a durable, actionable view of where costs are moving.

Optimize labor scheduling against actual demand. Align staffing levels with patient volume, acuity, and operational demand using predictive modeling. Reducing reliance on agency labor through better scheduling discipline—rather than cutting headcount—is where the greatest sustainable labor savings exist. At least 70% of health systems surveyed by Kaufman Hall are already pursuing widespread staffing optimization for this reason.

Strengthen revenue cycle management and billing accuracy. Billing errors, claim denials, and underpayment recovery failures are a hidden revenue leak for healthcare organizations. Improving coding accuracy, denial management workflows, and payer contract adherence can recover significant lost revenue without requiring operational cuts. Electronic prior authorization standards alone could save $515 million annually and 14 minutes per authorization (CAQH).

Strategies That Reduce Costs by Changing the Operational Context

These restructure how administrative functions are resourced, how vendor relationships are governed, and how organizational scale is leveraged.

Deploy offshore capability centers for administrative, analytics, and procurement functions. Many healthcare organizations—particularly PE-backed providers and mid-market health systems—are shifting high-volume, process-driven functions such as revenue cycle support, procurement analytics, financial reporting, and spend management to offshore capability centers. This model blends domain expertise with labor cost efficiency, allowing onshore teams to focus on strategic and patient-facing work.

Colab91 has built this model for Pediatric Associates (a TPG portfolio company) and Kindred Healthcare, scaling India-based teams for strategic sourcing and analytics.

For PE sponsors managing multiple healthcare portfolio companies, a shared offshore delivery model enables cross-portfolio procurement programs that individual entities couldn't fund or staff on their own.

Redesign pharmacy benefit management for transparency and governance. Move away from opaque PBM relationships by adopting transparent formulary governance, biosimilar substitution programs, and class-specific policies for GLP-1s and specialty biologics. This requires active contract management and formulary oversight—not just vendor selection. Organizations that treat PBM contracts as set-and-forget arrangements routinely overpay on specialty drug spend by 15–30%.

Build direct contracting relationships to reduce network dependency. Large employers and self-funded healthcare operators can bypass traditional network markups by contracting directly with high-quality providers for high-cost procedures. Pair this with strong utilization management and payment integrity programs to control realized costs, not just contracted rates. Direct contracting only creates value when the utilization discipline is in place to prevent volume from offsetting the rate advantage.

Conclusion

Healthcare costs in 2026 don't require acceptance—they require understanding. The organizations managing costs most effectively are doing so by addressing where costs actually originate: upstream decisions about care models and procurement, operational gaps that allow spend to drift, and structural inefficiencies in how administrative and analytical functions are resourced.

Cost reduction that sticks is built into how an organization operates day-to-day — not triggered by a bad quarter. Organizations that embed procurement discipline, spend visibility, and analytical rigor into their operating model are consistently better positioned to protect margins and improve care quality over time. For healthcare providers looking to build those capabilities without proportional headcount growth, dedicated offshore procurement and analytics teams offer a practical path forward.

Frequently Asked Questions

What are the key components of healthcare cost reduction strategies?

Effective healthcare cost reduction operates across three layers: upstream decisions (plan design, procurement strategy), operational management controls (spend analytics, staffing models, revenue cycle discipline), and structural changes (network design, vendor accountability). Sustained impact requires all three working together.

What are healthcare cost trends for 2025 and 2026?

PwC projects a 9% commercial medical cost trend for 2026-2027—the highest in nearly two decades. Primary drivers include pharmacy spend (especially GLP-1s and specialty biologics), labor inflation, provider consolidation driving up reimbursement rates, and sustained behavioral health utilization growth.

How can healthcare organizations reduce labor costs without compromising care quality?

Demand-aligned staffing models reduce dependency on agency and contract labor through better scheduling discipline. Shifting non-clinical administrative functions (procurement reporting, spend analytics, revenue cycle support) to more cost-efficient delivery models frees clinical labor budget for direct patient care.

What role does procurement play in healthcare cost reduction?

Strategic sourcing and spend analytics help healthcare organizations consolidate vendor relationships, improve contract compliance, and eliminate uncontrolled third-party spend that accumulates invisibly across supply chains. For PE-backed organizations, portfolio-wide procurement programs multiply those savings across all acquired entities simultaneously.

How are PE-backed healthcare companies approaching cost reduction differently?

PE-backed healthcare organizations are prioritizing portfolio-wide spend consolidation, offshore capability centers, and data-driven procurement analytics to create enterprise value across acquired entities. Negotiating as a unified portfolio unlocks pricing that standalone entities cannot access.

What is the biggest driver of healthcare cost increases in 2026?

Pharmacy spend—particularly GLP-1s priced above $1,000 per month and specialty biologics—and labor inflation are the largest near-term drivers. Provider reimbursement pressure from consolidation and growing administrative complexity from prior authorization and denial management compound these costs over time.