Introduction

PE firms face a familiar squeeze: compressed hold periods, rising deal competition, and limited room to grow returns through leverage alone. Revenue initiatives take time and carry execution risk. Financial engineering has largely played out. What remains - and what many sponsors still underutilize - is procurement optimization.

The math is straightforward. Every dollar saved in procurement drops directly to EBITDA, with no incremental headcount, no marketing spend, no cost-of-goods headwinds. At prevailing exit multiples, even modest savings compound into meaningful equity value.

This article covers why procurement ranks among the highest-return levers available to PE sponsors, which tools drive the most impact, and how to sequence them across the deal cycle. It also examines how Colab91 - whose leadership has delivered procurement transformation at portfolios backed by Carlyle Group and TPG - helps PE-backed companies build the capability to execute.

Key Takeaways

- Procurement savings flow directly to EBITDA and multiply at exit , delivering more capital-efficient returns than most revenue initiatives

- Core tools include spend analytics, e-sourcing, contract management, supplier performance platforms, and AI-powered forecasting

- Start during due diligence - A&M research shows up to 70% of indirect savings can be captured in year one

- Spend aggregation and GPOs across the portfolio multiply savings no single company can achieve independently

- Most mid-market PE-backed companies lack mature procurement functions; offshore capability centers close that gap faster than hiring onshore

Why Procurement Is One of the Highest-Return Value Creation Levers in Private Equity

The Core Economics

Procurement savings have a property other value creation levers don't: they bypass income statement friction entirely. Revenue growth requires sales effort, marketing spend, and often added COGS. Procurement savings don't. They go straight to EBITDA.

PitchBook reports median EV/EBITDA for buyouts above $1B reached 15.5x in 2024, with sub-$100M deals trading below 10x. At those multiples, even a modest EBITDA improvement translates to substantial equity value.

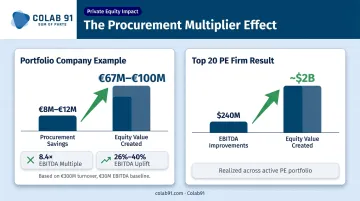

Efficio's modeling puts numbers to it: a European portfolio company with €300M in turnover and €30M EBITDA that generates €8M–€12M in procurement-driven improvement creates €67M–€100M in equity value at an 8.4x multiple - a 26%–40% EBITDA uplift from procurement alone. The same research documents a Top 20 global PE firm realizing over $240M in EBITDA improvements, translating to roughly $2B in equity value.

From Back Office to Boardroom

For most of corporate history, procurement was treated as a transactional function - paper-pushers managing purchase orders. Leading PE sponsors have fundamentally reframed it. Firms like Blackstone, KKR, and TPG now embed procurement as a first-100-days priority alongside revenue growth and operational improvement - not deferred to year two.

McKinsey's research supports this shift: GPs focused on asset operations achieve IRRs 2–3 percentage points higher on average than peers who don't.

What PE Firms Actually Inherit at Acquisition

Most mid-market acquisitions come with the same procurement problems:

- No spend visibility - leadership can't tell you who they're buying from or at what prices across categories

- Expired or missing supplier contracts - value leaking through unenforced terms and auto-renewals

- Tail spend sprawl - dozens of low-value suppliers consuming disproportionate management attention

- Fragmented processes - decentralized buying with no policy enforcement and minimal compliance tracking

These aren't weaknesses to flag in the CIM. They're the opportunity. Procurement tools are designed to address exactly these gaps - and do it fast enough to matter within a 3–7 year hold period.

Key Procurement Tools PE Firms Use to Drive Portfolio Returns

No single tool does everything. PE firms deploy a layered stack, each handling a specific job in the value creation workflow.

Spend Analytics Platforms

Before any sourcing event, contract negotiation, or supplier consolidation effort can begin, the team needs visibility. Spend analytics platforms aggregate and classify expenditure data across categories, suppliers, and business units, creating the baseline that makes all other procurement work evidence-based rather than directional.

The best platforms surface:

- Supplier fragmentation and duplication across categories

- Tail spend concentration (where 80% of transactions often represent less than 20% of total spend)

- Renegotiation opportunities where pricing hasn't been benchmarked in years

- Categories ripe for consolidation or competitive bidding

A&M estimates that cloud and AI-based spend analytics can positively impact roughly 75% of indirect spend in PE procurement programs. Without this foundation, sourcing initiatives are guesswork.

Colab91's AI-powered spend analytics product addresses exactly this gap - generating spend visibility and opportunity identification for mid-market and PE-backed companies that rarely have this capability in place at close.

Strategic Sourcing and E-Sourcing Tools

Once spend is visible and categorized, e-sourcing tools allow portfolio companies to run competitive bidding events - reverse auctions, RFP automation, supplier benchmarking - faster and at greater scale than traditional manual approaches.

The timing advantage matters enormously. A&M's research shows up to 20% of indirect savings can be captured within the first 100 days. Category wave planning, which sequences sourcing initiatives by savings potential and implementation speed, is what enables PE teams to stack quick wins early and build momentum for more complex categories later.

Contract Management Systems

Acquired companies frequently have supplier relationships running on expired agreements, auto-renewing at unfavorable rates, or with compliance terms that exist on paper but aren't enforced. Contract lifecycle management (CLM) tools fix this systematically.

WorldCC research shows poor contract management loses almost 9% of contract value annually on average, with worst performers losing 15% or more. In a PE context, CLM hygiene also has a second benefit: clean contracts, documented renewals, and enforced terms all signal to potential buyers that the business is well-run.

Supplier Performance Management Tools

Negotiating savings and realizing savings are two different things. Supplier performance platforms track on-time delivery, quality, and cost adherence to ensure contracted rates are actually flowing through to the P&L. For companies pre-acquisition that have been managing supplier relationships reactively, this category often delivers the most immediate compliance lift.

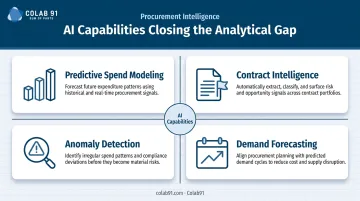

AI-Powered Analytics and Forecasting

The most immediate AI application in procurement is automating analysis that previously consumed significant analyst hours. Smaller teams can now operate at an analytical level that once required much larger headcount. Key capabilities include:

- Predictive spend modeling to forecast category costs and budget variances

- Contract intelligence that flags renewal dates, pricing escalators, and non-standard terms

- Anomaly detection that surfaces billing errors and off-contract spend

- Demand forecasting to align procurement timing with actual business needs

Gartner reported in 2024 that 73% of procurement leaders expected to adopt GenAI by year-end 2024. For PE-backed teams that are lean by design, these tools close the analytical gap without adding headcount.

How to Deploy Procurement Tools Across the PE Deal Cycle

Which tools you choose matters less than when you deploy them. A phased approach aligned to the deal cycle is what separates PE firms that capture procurement savings early from those that start implementing in year three.

Pre-Acquisition: Due Diligence

Spend analytics and supplier contract review should begin before close - not after. During due diligence, PE teams should assess:

- Procurement maturity - what percentage of spend is under active management?

- Supplier concentration risk - are there single-source dependencies that create operational risk?

- Contract coverage - what percentage of spend is governed by formal, current agreements?

- Quick-win identification - which categories are immediately competitive-biddable?

This work serves two purposes: it informs deal valuation (including where to flag risk), and it creates a procurement roadmap that can be activated on day one rather than designed from scratch after close.

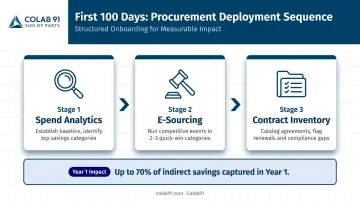

First 100 Days Post-Acquisition

This window is the highest-leverage period in the hold. Organizational change resistance is lower, leadership attention is focused, and credibility earned through early wins funds the mandate for larger transformation.

Priority deployment sequence:

- Spend analytics - establish the baseline and identify the top categories by savings potential

- E-sourcing - run competitive events in 2–3 quick-win categories immediately

- Contract inventory - catalog all supplier agreements, flag renewals and compliance gaps

A&M's research shows up to 70% of total indirect savings can be captured within the first year - which means the foundation built in the first 100 days directly determines the scale of year-one returns.

Steady-State Optimization

Once the foundation is in place, the goal shifts from rapid deployment to building lasting capability. A mature procurement operating model runs continuous sourcing waves, tracks supplier performance against contracted terms, and uses AI tools to flag emerging opportunities without manual intervention.

This is also when cross-portfolio strategies become viable. PE firms can aggregate spend data across portfolio companies and run joint sourcing initiatives wherever categories overlap - compounding savings that no single portfolio company could achieve alone.

Exit Readiness

A well-documented procurement function accelerates buyer confidence. Acquirers want to see that cost savings are structural - not dependent on a few key people or informal supplier relationships.

Before exit, PE firms should confirm:

- Supplier contracts are current, clean, and transferable

- Savings are validated against actual P&L impact, not just projected

- The operating model is scalable without the current deal team's involvement

- A clear savings narrative is built into the value creation plan

This documentation doesn't just support valuation - it shortens diligence cycles and reduces negotiation friction.

Cross-Portfolio Procurement Strategies That Multiply Savings

Individual portfolio company procurement hits a ceiling quickly. Cross-portfolio strategies raise that ceiling by creating scale no single company can generate alone. Three approaches consistently move the needle.

Spend Aggregation

Pooling volume across portfolio companies in related categories - packaging, logistics, MRO, IT, professional services - unlocks enterprise-level pricing that individual companies simply can't reach. This requires a portfolio-level spend visibility layer, typically built on a shared analytics platform. Firms like Colab91 build and operate those platforms as part of their offshore procurement capability model, giving PE sponsors a unified view of where spend is concentrated and where leverage exists.

Group Purchasing Organizations (GPOs)

GPOs give mid-market portfolio companies access to pre-negotiated supplier rates in indirect categories where their individual spend wouldn't move the needle. Blackstone, KKR, and TPG have documented savings through GPOs such as CoreTrust - harmonizing pricing across portfolio companies in categories that would otherwise be purchased independently at higher rates.

Supplier Consolidation

Reducing supplier fragmentation across the portfolio strengthens key vendor relationships and enables performance management at a scale that makes suppliers take commitments seriously. The practical results:

- Fewer suppliers means less administrative overhead per company

- Consolidated volume improves negotiating leverage at renewal

- Shared supplier scorecards create accountability across the portfolio

Building the Procurement Capability PE-Backed Companies Actually Need

Tools are necessary but not sufficient. The companies that realize the most procurement value aren't just the ones that buy the right software - they're the ones that have the right team to operate it.

The Capability Gap in Mid-Market PE

Most mid-market acquisitions come with a procurement function in name only - perhaps one or two buyers managing transactions, no strategic sourcing capability, no analytics, and no structured supplier management. The gap isn't just a tool gap; it's a talent gap. And that gap has real consequences: without the right team, spend analytics sits uninterpreted, sourcing events don't get run, and contract compliance doesn't get tracked.

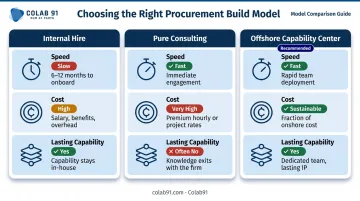

The Build Options

| Option | Speed | Cost | Lasting Capability |

|---|---|---|---|

| Internal hire | Slow (6–12 months) | High | Yes |

| Pure consulting | Fast | Very high | Often no |

| Offshore capability center | Fast | Sustainable | Yes |

Internal hiring is too slow for PE timelines and costly in competitive US markets. Pure consulting builds dependency, not capability - and the fees accumulate quickly across a 5-year hold period. The offshore capability center model addresses both constraints: domain-expert talent at sustainable cost, with the team genuinely dedicated to the portfolio company rather than billing hours on rotating engagements.

The Talent-Plus-Technology Combination

Colab91's model for PE-backed companies is built on this premise. The firm establishes India-based procurement and analytics teams - recruiting domain specialists in strategic sourcing, spend analytics, and supplier management - that serve as the operational engine behind the tools the portfolio company deploys.

A procurement tool without a capable team is just software. What creates actual value is a team that interprets spend data, designs sourcing events, manages supplier relationships, and tracks savings against the value creation plan week over week. Colab91 Managing Partner Madhur Kabra spent 16+ years scaling exactly this kind of operation at Impendi (later acquired by Accenture), serving PE sponsors including Carlyle Group and TPG.

Advisor Erika Jung brings the client-side perspective: she served as CPO at Pediatric Associates (a TPG portfolio company), leading enterprise-wide cost transformation from the inside. That combination of offshore operational depth, PE-specific domain expertise, and technology built for mid-market spend environments is what closes the capability gap within a PE hold period - not after it.

Frequently Asked Questions

What is the 80/20 rule in private equity procurement?

The 80/20 principle in PE procurement refers to the fact that roughly 20% of spend categories or suppliers typically account for 80% of total expenditure. Spend analytics platforms surface this concentration quickly, allowing PE teams to sequence sourcing initiatives toward the highest-return categories first.

What are the five procurement strategies PE firms use?

The five core strategies are:

- Strategic sourcing - competitive bidding and market leverage

- Spend consolidation - reducing supplier fragmentation

- Supplier relationship management - performance tracking and collaboration

- Tail spend management - controlling low-value transactions at scale

- Category management - structuring spend by category with dedicated ownership and strategy

When should a PE firm start implementing procurement strategies in a portfolio company?

Procurement assessment should begin during due diligence, prior to close. Formal implementation should start within the first 100 days post-acquisition, when organizational alignment is highest and early wins build the credibility needed to drive larger transformation through the hold period.

How does procurement improvement directly affect EBITDA?

Procurement savings reduce the cost of goods and indirect spend without requiring additional revenue or incremental headcount - dropping directly to EBITDA. At current market multiples, even a $5M EBITDA improvement can translate to $50M–$75M in equity value at exit, depending on deal size and sector.

What procurement tools do PE firms typically use?

The core stack includes spend analytics platforms, e-sourcing tools, contract lifecycle management (CLM) systems, supplier performance management platforms, and AI-powered forecasting tools. Results improve significantly when deployed as an integrated stack with a capable team behind them, not as standalone point solutions.

How can mid-market PE-backed companies build procurement capability without large teams?

Most mid-market PE-backed companies address the capability gap through offshore procurement and analytics capability centers - accessing domain-expert talent at a fraction of US onshore hiring costs, with the ability to stand up functional teams in weeks rather than months to match PE execution timelines.