Introduction

Picture this: it's month-end, and you're pulling the latest spend report. Two departments are already over budget — not because anyone made a rogue purchase last week, but because vendor agreements signed three weeks ago never triggered a financial record until the invoice landed in AP. The data isn't wrong. It's just late.

According to a 2023 Pigment survey reported by CFO.com, nearly 89% of CFOs and finance leaders make decisions based on inaccurate or incomplete data on a monthly basis. That's not a reporting problem — it's a structural one.

Real-time spend visibility means surfacing what a company has committed to spend — before the invoice arrives, not after. That requires upstream controls, clean data pipelines, and analytics built for committed spend, not just billed spend.

This guide covers what that infrastructure looks like, why mid-market and PE-backed companies are still catching up, and the steps CFOs are taking to close the gap.

Key Takeaways

- Real-time spend visibility means tracking committed spend and incurred spend together — most finance systems only capture the latter.

- The gap is structural: informal purchases create a 20–30 day blackout before finance sees the data.

- Closing the gap requires three layers: upstream spend controls, data integration, and analytics capability.

- Tools alone don't solve it. The analytics talent to interpret spend data is often the missing piece.

- For PE-backed companies, committed spend reporting is increasingly part of standard financial governance.

What Real-Time Spend Visibility Actually Means

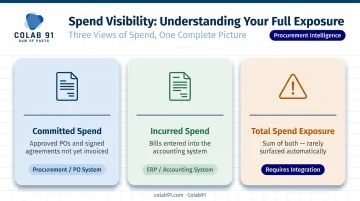

Real-time spend visibility is the ability to see, at any point during the month, every dollar the company has committed to spend — including approved purchase orders not yet invoiced — alongside what has already been billed and recorded.

That definition matters because of what it excludes.

A faster ERP dashboard is not real-time spend visibility. Refreshing a report that only captures invoiced expenses more frequently just shows the same incomplete picture on a shorter delay. The distinction between spend reporting and spend visibility comes down to one question: does your system know about a spending commitment the moment it's approved, or only when the vendor sends a bill?

The Two Numbers Every CFO Needs

| Metric | What It Captures | Where It Lives |

|---|---|---|

| Committed Spend | Approved POs, signed agreements, open vendor contracts not yet invoiced | Procurement/PO system |

| Incurred Spend | Invoices entered into the accounting system | ERP / accounting system |

| Total Spend Exposure | The sum of both | Rarely surfaced automatically |

Most accounting systems — QuickBooks, NetSuite, Sage Intacct — are designed to record what happened. As Oracle NetSuite's own documentation notes, purchase orders list "what has been ordered, not necessarily what you've bought and paid for" and sit in a non-posting account that doesn't directly affect financial balances.

The committed spend layer isn't a native financial object in most accounting systems without additional configuration.

Why Most CFOs Are Still Operating in the Dark

The typical purchase in a mid-market company unfolds something like this: a department head contacts a preferred vendor, places an order informally or via email, the invoice arrives two to three weeks later, and gets coded by AP.

From spending decision to CFO visibility: potentially 20–30 days.

That lag is structural, not accidental.

How Organizational Growth Makes It Worse

At smaller headcounts, informal visibility is manageable. A CFO at a 50-person company can reasonably know what's being bought through direct conversation. Once a company scales past 100–200 employees across multiple departments or geographies, that informal channel breaks down entirely — and committed spend becomes structurally invisible.

Why Accounting Systems Can't Fix This Alone

ERPs and accounting tools are built to record what happened. They capture incurred spend through invoices. Purchase orders, where supported at all, typically lack approval workflows and budget-checking at the point of request.

Intuit's QuickBooks support documentation confirms that a purchase order is a non-posting transaction — it does not affect accounting until a bill is created from it. That means the commitment has already been sitting off the books for weeks before finance sees it.

Three structural gaps compound this problem:

- ERPs record history, not intent — committed spend never appears until invoiced

- PO workflows, where they exist, rarely enforce budget checks at the request stage

- Approval chains live in email or verbal agreements, leaving no auditable trail

Why AP Automation Isn't the Answer Either

AP automation tools begin their work when the invoice arrives — which is already after the spending commitment has been made. They address processing delays effectively. According to Ardent Partners' State of ePayables 2024, the gap between best-in-class and average AP performance is significant:

| Metric | Best-in-Class | Average |

|---|---|---|

| Invoice processing time | 3.1 days | 17.4 days |

| Cost per invoice | $2.78 | $12.88 |

That's a real efficiency gain — but it does nothing to surface the committed spend that existed weeks before that invoice was generated.

The PE-Specific Pressure

Committed spend invisibility isn't just an operational nuisance — for PE-backed portfolio companies, it's a governance problem. Sponsors and operating partners increasingly require reporting that reflects total spend exposure, committed and incurred, as part of standard board-level oversight. Budget variance analysis built only on invoiced data routinely understates where a company actually stands mid-period — sometimes by a significant margin when large purchase orders are in flight.

How CFOs Build Real-Time Spend Visibility

Achieving real-time spend visibility requires three interconnected layers. Fixing only one produces partial visibility at best.

Upstream Spend Controls

Visibility starts before the invoice — at the moment a spending decision is made. Every purchase above a defined threshold needs to go through a formal request-and-approval process that creates a documented financial record at the point of approval. Without that, committed spend remains invisible until the vendor sends a bill.

A practical approach most CFOs use:

- Route the top 20% of purchases by dollar value through senior finance approval — this typically covers the majority of total spend

- Lower-value purchases go automatically to department heads, keeping the process lean

- A written purchasing policy sets the foundation: which purchases require a PO, what the dollar thresholds are, and who approves what

The policy doesn't need to be complex. A single document covering thresholds, approval authority, and vendor guidelines is the prerequisite for any software solution to function correctly.

That policy gap has a measurable cost. Ardent Partners found that only 61% of invoices are linked to a PO on average, while best-in-class AP organizations reach 83.7%. The difference in PO coverage maps directly to the committed spend finance teams cannot see.

Data Integration and the Open PO Report

Once purchase orders exist as formal records, they need to feed into a system connected to the accounting infrastructure in real time. This makes committed spend visible against departmental budgets the moment a request is approved, weeks before the invoice arrives.

The Open PO Report is the CFO's primary instrument for committed spend visibility. It should contain:

- Vendor name

- PO amount

- Amount invoiced to date

- Remaining commitment

- Budget code and department

Three-way matching completes the picture: when a purchase order, goods receipt, and invoice align automatically, manual reconciliation drops and the audit trail from approval to payment stays clean. Ardent reports that 81% of best-in-class organizations have two- or three-way matching capabilities, versus 69% of all others — a gap that correlates directly with processing efficiency and exception rates.

Analytics and Reporting Layer

Data integration creates the raw material. Turning that into decisions is the job of the analytics layer.

This layer is responsible for:

- Budget variance reports by department

- Supplier concentration analysis

- Category-level spend breakdowns

- Threshold-driven alerts when committed spend in a category approaches its budget limit

Most mid-market companies underinvest here. They acquire a spend management tool but lack the analytical capability to extract strategic value from it.

The threshold-driven alert feature is the most underused example. Rather than waiting for a month-end report, a CFO can configure an alert that fires automatically when a department's committed spend hits 80% of budget. That single setting shifts finance from reactive reporting to proactive monitoring.

What Changes When Visibility Is in Place

Budget Conversations Shift Direction

Before: On the 28th, the CFO reviews a month-end report and discovers marketing overspent by $40,000. The invoices have been processed, the contracts signed, the work delivered. The conversation is about what happened.

After: On the 12th, an alert fires. Committed spend in marketing has hit 78% of the monthly budget with three vendor agreements still open. The CFO calls the department head before the next PO is issued. The conversation is about what's going to happen.

Real-time visibility makes that shift possible — and it ripples across every core finance function.

Cash Flow Forecasting Gets Traction

When open purchase orders are visible alongside outstanding invoices, finance teams can model:

- When cash will need to move based on committed obligations

- Which vendors are approaching payment due dates

- How much liquidity buffer the business actually needs

Cash flow planning becomes a forward-looking model — not a reconciliation exercise run after the fact.

Month-End Close Accelerates

When every purchase has a documented approval record and every invoice is matched automatically to a PO and receipt, the manual reconciliation that extends close cycles shrinks considerably. A 2025 survey by CFO.com found that 50% of finance teams still take six or more business days to close, with cross-team dependencies (56%) and Excel-driven processes (50%) cited as the top barriers. PO-based procurement with automated matching directly reduces both of those friction points.

Board and Investor Reporting Matures

For PE-backed companies, real-time spend visibility means CFOs can report total spend exposure rather than trailing invoiced spend. That's a stronger, more auditable signal of financial control — and it matters for audit preparation, covenant compliance, and demonstrating operational discipline to sponsors at quarterly reviews.

The Analytics Capability Gap: Why Data Alone Is Not Enough

Many mid-market companies successfully implement spend management software and ERP integrations, then find they still can't generate consistent, actionable spend analytics. The reason is rarely the tool — it's a talent gap.

The analytical work required to produce category-level spend analysis, supplier benchmarking, and budget variance interpretation requires dedicated expertise that most mid-market finance teams don't have in-house. This function sits at the intersection of finance and procurement. It's distinct from AP processing (transactional, invoice-focused) and from strategic finance (P&L and FP&A-focused). It requires its own skill set.

Deloitte's 2025 Chief Procurement Officer Survey found that talent gaps were cited as a barrier to value delivery by 34% of CPOs surveyed — alongside technology capability (40%) and siloed ways of working (57%). The same survey found that 64% of CPOs ranked greater supply chain and spend visibility as one of the top three most effective risk-mitigation strategies. The ambition is there. The capability to execute on it often isn't.

What This Analytics Capability Actually Looks Like

Productive spend analytics goes well beyond standard reporting. It requires:

- Cleansing and categorizing raw spend data to a consistent taxonomy

- Identifying off-contract and maverick spend patterns

- Benchmarking supplier pricing against market rates

- Building spend cubes that enable multi-dimensional category analysis

- Producing board-ready narrative analysis that CFOs can present with confidence

How Mid-Market Companies Are Solving It

Rather than building an in-house analytics team at full cost, more companies are turning to dedicated offshore capability centers that deliver domain expertise at a sustainable cost structure. Colab91 works with mid-market and PE-backed companies — including portfolio companies of Carlyle Group, TPG, Elliott, and BC Partners — to build India-based teams that specialize in procurement analytics and spend intelligence.

The model combines AI-augmented analytics with dedicated human analysts who deliver weekly and monthly intelligence packages. Core capabilities include:

- Spend cube construction and multi-dimensional category analysis

- Off-contract spend identification and maverick spend tracking

- Supplier concentration analysis

- Working capital and payment-terms analytics

For PE portfolio companies, Colab91's teams produce the board-ready procurement reporting that sponsors increasingly expect as part of standard financial governance — at a cost structure that works for companies without the budget for a fully onshore analytics function.

Colab91's leadership team previously scaled these capabilities at Impendi (subsequently acquired by Accenture), building multifunctional offshore teams for PE sponsors and their portfolio companies across Carlyle, TPG, and BC Partners.

Frequently Asked Questions

What are the three most important qualities of a CFO?

Strategic foresight, financial discipline, and the ability to translate data into decisions. Real-time visibility into company spending is foundational to all three — a CFO working from last month's invoices cannot plan forward with confidence or credibly present financial position to a board.

What is the difference between committed spend and incurred spend?

Committed spend is money a company has agreed to pay — through approved purchase orders or signed vendor agreements — but has not yet been invoiced for. Incurred spend is what has been invoiced and recorded in the accounting system. Total spend exposure requires both numbers together.

Why do most CFOs still lack real-time visibility into company spending?

The root cause is structural. When purchases happen without formal approval processes, committed spend stays invisible until the invoice arrives, often 20–30 days after the spending decision was made. Accounting systems record invoiced transactions, not approvals, so the gap persists until upstream controls are in place.

What is an Open PO Report and why does it matter for CFOs?

An Open PO Report shows every approved purchase order sent to a vendor that has not yet been fully invoiced — including remaining commitment amounts and budget codes. It gives CFOs a real-time view of committed spend that accounting systems alone cannot surface.

Can AP automation tools give a CFO real-time spend visibility?

No. AP automation tools begin their work when the invoice arrives — after the spending commitment has already been made. They improve invoice processing speed and reduce exceptions, but they don't capture committed spend upstream. The visibility gap remains.

How can mid-market companies build spend analytics capability without a large in-house team?

One proven model is a dedicated offshore analytics function that pairs procurement and spend analytics expertise with cost-efficient offshore delivery. This gives mid-market CFOs the analytical depth they need without the fixed cost of a fully onshore team.