Introduction

According to CPO Rising's 2025 benchmark, procurement teams now manage roughly 71% of total enterprise spend - meaning close to 29% sits outside any formal procurement oversight. For PE-backed companies, that unmanaged portion isn't just a procurement inefficiency. It's an EBITDA problem.

Every dollar that flows through unapproved vendors, auto-renewed contracts, or fragmented indirect categories compresses the margins that determine exit valuation. With median PE purchase multiples reaching 11.8x EBITDA in 2025, even modest EBITDA leakage carries significant enterprise value consequences. Holding periods now average close to seven years - but the pressure to demonstrate run-rate improvement well before exit hasn't eased.

This guide covers three things: how spend costs actually accumulate in PE-backed companies, what drives them structurally, and three distinct categories of strategies to reduce them. The right strategy depends heavily on where a portfolio company sits in the investment lifecycle, and this guide helps you determine which levers apply.

Key Takeaways

- ~29% of enterprise spend sits outside procurement management; indirect categories alone represent 20–40% of total spend

- Cost problems in PE-backed companies are structural, not transactional - they stem from missing visibility, decentralized buying, and no procurement accountability

- Three cost-reduction levers exist: changing decisions, improving management visibility and governance, and restructuring the operating model

- Durable savings require repeatable procurement capability built to last across the full holding period, not one-off sourcing events

How Spend Costs Typically Build Up in PE-Backed Companies

Unmanaged spend costs rarely announce themselves. They don't appear as a single line item on an income statement - they accumulate gradually, category by category, quarter by quarter.

The typical pattern starts at acquisition. A newly acquired business arrives with inherited vendor contracts that were never competitively sourced, auto-renew annually, and haven't been reviewed against current needs. The acquiring PE firm is focused on integration, leadership transitions, and the first 100-day plan. Procurement governance rarely makes the critical path.

Why Fragmentation Makes It Worse

From there, cost build-up becomes compounding:

- Department heads in IT, HR, facilities, and operations buy independently - with no visibility into what adjacent teams have already negotiated

- Without consistent spend classification by category, supplier, and business unit, overpayments stay buried in accounts payable data

- Indirect categories like software, logistics, and professional services expand as the business grows, but rarely attract the same scrutiny as direct spend

The true cost exposure only surfaces when someone intentionally looks through a structured spend diagnostic. Most portfolio companies never conduct one during the holding period. By exit, those costs have been quietly compounding for years.

Key Cost Drivers for PE Portfolio Spend

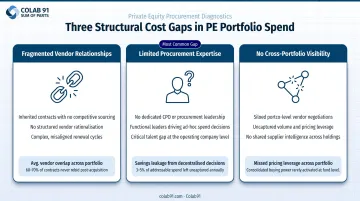

The structural cost drivers in PE-backed companies tend to cluster around three gaps rather than any single category:

Fragmented vendor relationships inherited at acquisition - Businesses built through organic growth or prior acquisitions typically carry dozens of vendor relationships in each major indirect category, many selected by default and few reviewed competitively. Each carries its own pricing, terms, and renewal cycle, making consolidation difficult without a structured sourcing review.

Limited procurement expertise at the portfolio company level - Only 14% of procurement leaders report having adequate talent to meet their function's future needs, according to Gartner. For mid-market PE-backed companies, the gap is sharper - many lack a dedicated CPO or category management function entirely, leaving spend decisions to functional leaders whose primary expertise is not procurement.

No cross-portfolio visibility - PE sponsors holding multiple portfolio companies in overlapping categories - IT infrastructure, HR services, logistics, professional services - rarely aggregate that spend into a coordinated buying position. Each portco negotiates alone, leaving significant pricing leverage uncaptured.

Why Timing Compounds the Problem

Decisions made in Year 1 of the hold period disproportionately shape the cost profile for the entire investment cycle. Categories left unreviewed during onboarding tend to remain unoptimized through exit.

The analysis also needs to be company-specific. A fragmented, recently acquired business has very different challenges than a mature platform company preparing for exit. Applying generic strategies to either scenario consistently underperforms.

Cost-Reduction Strategies for PE Spend Management

The right strategy depends on where the portfolio company sits in its investment lifecycle, what data is available, and whether the core problem is rooted in decisions made, controls in place, or structural factors in the operating model. These three levers address each of those root causes separately.

Strategies That Reduce Costs by Changing Decisions

These approaches target the procurement decisions made before or at the point of engagement: scope, vendor selection, category policy, and prioritization.

Run a spend diagnostic before any sourcing begins. Map all third-party spend by category and vendor within the first 90 days post-close. This baseline determines which categories belong in the value creation plan and which can wait - effort otherwise flows to visible spend rather than high-opportunity spend.

Challenge inherited indirect contracts from first principles. Rather than accepting existing terms, question whether each category is necessary at current volume, whether specs can be simplified, and whether the incumbent was selected competitively or by default. McKinsey estimates zero-based budgeting can identify 10–20% SG&A savings in under six months; Bain's ZBB research puts that range at 15–25% for programs executed with genuine structural discipline.

Reduce internal demand before negotiating price. McKinsey's PE-specific procurement research identifies a point that's easy to overlook: more than half of total savings potential often comes from noncommercial levers rather than price negotiation alone. That means:

- Harmonizing product ranges across business units

- Eliminating low-utilization software licenses

- Challenging legacy service commitments at current scope

Each of these reduces the cost base before any vendor discussion begins.

Set sourcing policies by category before contracts renew. Define approval thresholds, competitive process requirements, and strategic versus spot buying criteria for each category. This prevents cost leakage from decentralized decisions and ensures savings don't erode through subsequent maverick spend (purchases made outside approved channels).

Strategies That Reduce Costs by Changing How Spend Is Managed

These approaches target visibility, accountability, and analytical discipline during the active management period.

Build a unified spend data layer first. Normalize and classify spend data from accounts payable and procurement systems into a consistent taxonomy: by category, supplier, and business unit. Without this foundation, billing errors go undetected, consolidation opportunities stay invisible, and analytics produce noise instead of insight. Every other cost initiative depends on it.

Run structured vendor performance reviews quarterly. Reviews against commercial terms and SLA commitments serve two purposes: they surface billing errors and unused credits before expiry, and they shift the negotiating dynamic from reactive (renewal pressure) to proactive (relationship management). Vendors who know they're being tracked on a schedule behave differently than those who aren't.

Match procurement governance to organizational scale. Even a lean internal policy defining approval thresholds, preferred vendor lists, and category ownership dramatically reduces maverick spend. McKinsey reports that advanced analytics can reduce manual supplier-governance effort by 30–50% and enable indirect procurement savings of 15–20% through digital governance tools. Complexity isn't the goal; consistency is.

Rationalize tail spend fragmentation with analytics. A large share of indirect spend typically sits with tail vendors that generate disproportionate administrative burden relative to their commercial value. Consolidating or outsourcing management of that tail frees both cost and management attention for higher-value categories.

Strategies That Reduce Costs by Changing the Context Around Spend

These approaches address structural and external factors: the operating model, talent resources, and cross-portfolio relationships that either enable or constrain cost reduction.

Aggregate cross-portfolio buying power rather than leaving it on the table. When a PE sponsor holds multiple portfolio companies using the same categories, aggregating volume unlocks pricing tiers no individual company could access independently. Leaving each portco to manage vendors separately forfeits the leverage that portfolio scale provides. Group purchasing infrastructure, similar to what CoreTrust provides for multi-enterprise PE portfolios, can formalize this aggregation.

Redesign the operating model to remove complexity-driven cost. Businesses built through acquisition frequently carry duplicated functions, redundant back-office infrastructure, and legacy systems that inflate the indirect cost base. Renegotiating vendor contracts around that complexity provides temporary relief. Simplifying the structure, including rationalizing legal entities and consolidating back-office operations, reduces the cost base durably. McKinsey's post-merger vendor consolidation research points to 10–12% savings from intelligent spend consolidation alone.

Build persistent procurement capability rather than relying on one-time engagements. Episodic consulting engagements can identify savings, but they don't leave behind the data infrastructure, category expertise, or governance discipline needed to sustain them. The operating model choice determines whether gains hold.

Colab91 addresses this by establishing dedicated India-based procurement and analytics teams for PE sponsors and their portfolio companies, providing continuous spend intelligence and sourcing execution across the full holding period. The leadership team previously scaled a comparable model to 100+ practitioners serving Carlyle Group, TPG, Elliott, and BC Partners, which translates directly into pattern recognition on what persistent PE procurement capability requires.

Conclusion

Spend management costs in PE-backed companies are not inevitable. They result from structural gaps - missing visibility, fragmented buying, and absent procurement capability - that accumulate gradually and compound over time. Each of those gaps has a corresponding strategy.

Firms that capture the full EBITDA impact before exit rarely succeed because of better sourcing events. They succeed because they've built repeatable procurement capability that runs continuously across the holding period - not a post-close checklist item that gets deprioritized after the first 90 days.

With holding periods now averaging close to seven years and purchase multiples at 11.8x EBITDA, every point of sustainable cost improvement carries meaningful enterprise value. But only if it's captured early enough to show up in exit EBITDA.

Frequently Asked Questions

What is spend management in the context of private equity?

Spend management in PE refers to the strategic oversight and optimization of third-party expenditures across portfolio companies, with the goal of improving EBITDA margins and maximizing enterprise value over the holding period. It covers visibility, governance, analytics, and continuous cost optimization - well beyond a single sourcing event.

How does poor spend management affect EBITDA in PE-backed companies?

Unmanaged or fragmented spend erodes EBITDA through overpayments, missed consolidation opportunities, and undisciplined procurement decisions that compound over time. Because EBITDA is the primary driver of exit valuation, even modest improvements in the cost structure translate directly into enterprise value at the point of sale.

What are the highest-priority spend categories for PE firms to target?

Indirect categories - including IT/software, facilities, logistics, professional services, and HR/benefits - often receive the least procurement oversight in PE-backed companies, despite receiving far less governance attention than direct spend despite representing 20–40% of total expenditure, according to Deloitte.

How quickly can spend management initiatives deliver results in a PE portfolio?

Quick-win opportunities such as billing error recoveries, contract renegotiations, and license right-sizing can typically be surfaced within the first 60–90 days post-close by a focused procurement team. Structural improvements like operating model simplification and cross-portfolio leverage typically take 6–18 months to fully materialize in run-rate EBITDA.

What is the difference between strategic sourcing and spend management?

Strategic sourcing is a subset of spend management - it's the structured process of selecting and contracting vendors in specific categories. Spend management is the broader practice that includes visibility, governance, analytics, and ongoing optimization across all expenditure, not just the sourcing events.

How can PE firms build sustainable spend management capability without overloading portfolio company teams?

The most scalable approach is to augment lean internal teams with dedicated offshore procurement and analytics resources that bring both domain expertise and data infrastructure. This gives each portfolio company access to deep procurement capability without the cost and complexity of building a full in-house function from scratch at every company in the portfolio.